Massachusetts Reserve Study Requirements (2026)

Massachusetts does not require reserve studies by statute, but Chapter 183A, Section 10(i) mandates that every condominium in the Commonwealth maintain an "adequate replacement reserve fund" in a separate, segregated account. For the thousands of condo and HOA boards across Boston, Worcester, Springfield, Cambridge, and beyond, understanding what the law does — and does not — require is the first step toward responsible financial stewardship.

This guide covers what Chapter 183A requires, how lender rules create a de facto study mandate, Massachusetts-specific climate factors that shorten component lifespans, pricing, and a step-by-step compliance roadmap.

Legislation Links

Mass. General Laws Chapter 183A, Section 10

Mass. General Laws Chapter 183A, Section 1

Mass.gov — Official annotated text of Chapter 183A, §10

Are reserve studies required in Massachusetts? No. Massachusetts does not mandate reserve studies for condominiums or HOAs. However, Chapter 183A, Section 10(i) requires all condominiums to maintain an "adequate replacement reserve fund" in a separate, segregated account. A professional reserve study is the standard way to determine whether that fund is adequate.

What does "adequate" mean under Chapter 183A? The statute does not define a specific dollar amount or percentage. Adequacy depends on your community's components, their remaining useful lives, and estimated replacement costs. Most reserve professionals recommend a full study to quantify what "adequate" means for your specific property.

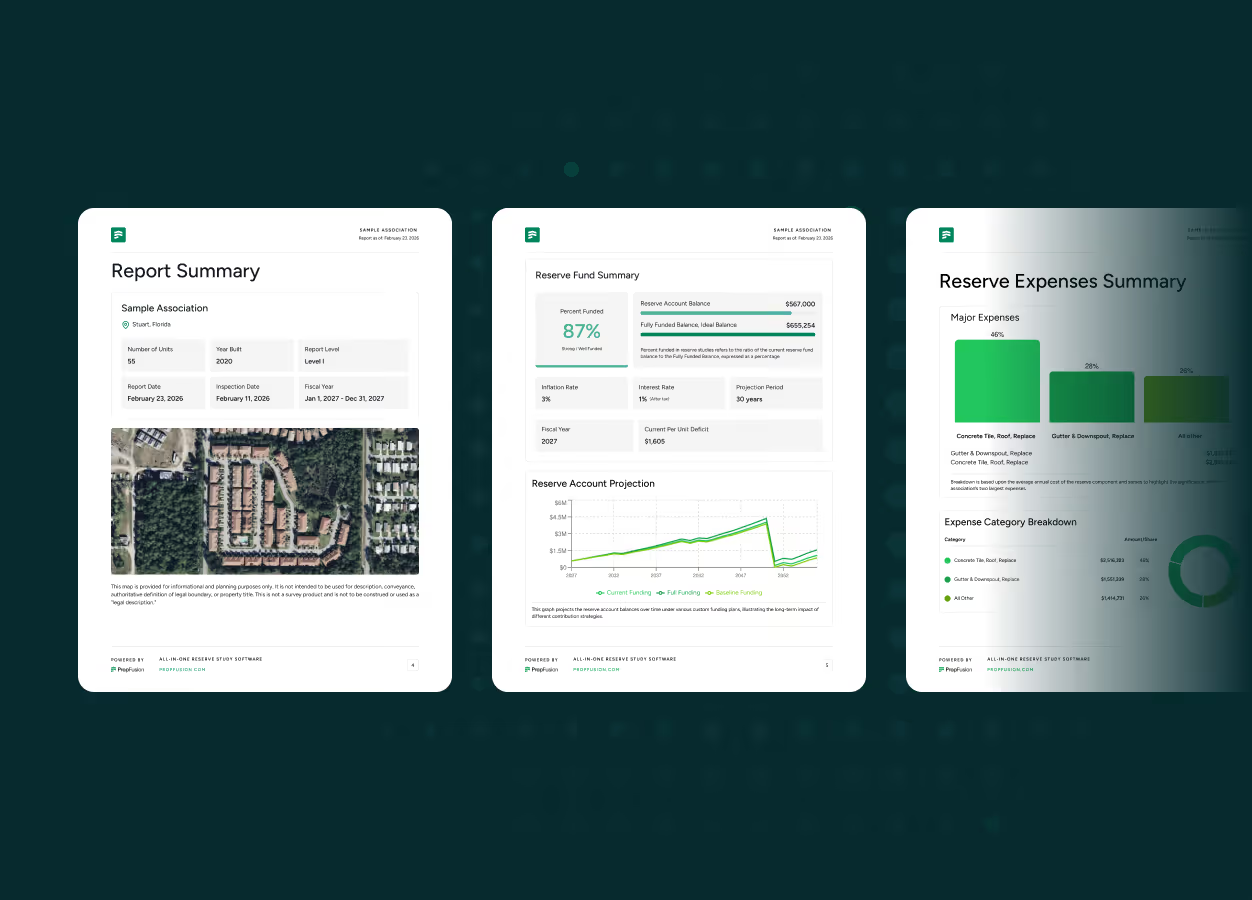

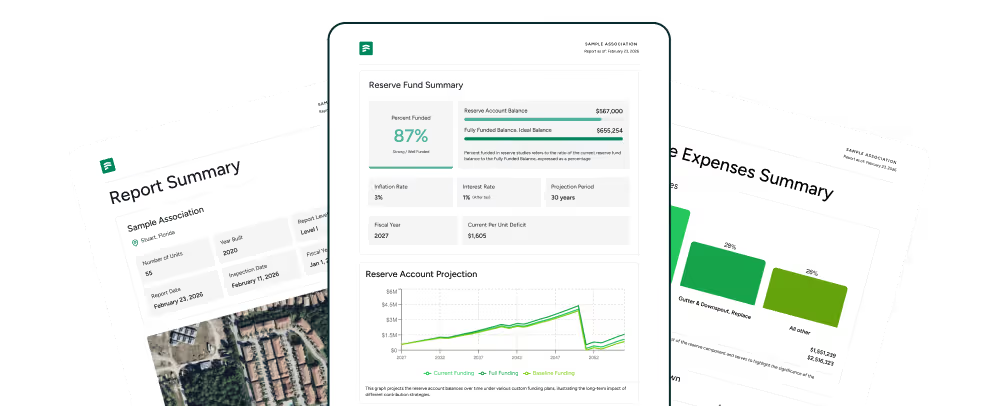

How much does a reserve study cost in Massachusetts? Professional reserve studies in Massachusetts typically range from $2,500 to $10,000. Greater Boston properties tend toward the higher end due to building complexity and elevated labor rates. Suburban and western Massachusetts communities generally fall in the lower-to-mid range.

PropFusion delivers professional reserve studies with 30-year funding plans - powered by modern technology and backed by certified reserve analysts.

Reserve studies vs. reserve fund laws in Massachusetts

A key source of confusion in Massachusetts is the difference between "reserve study requirements" and "reserve fund requirements." Multiple national and Massachusetts-specific sources confirm that:

- There is no Massachusetts statute that requires HOAs or condominium associations to commission reserve studies.

- All condominiums in Massachusetts are legally required to maintain an adequate replacement reserve fund, collected as part of the common expenses and deposited in a separate, segregated account.

For HOAs that are not structured as condominiums, there is no parallel statewide reserve statute. Their obligations come from declarations, bylaws, and the board's fiduciary duty to manage common property prudently.

In practice, most larger Massachusetts HOAs adopt reserve policies and studies similar to condominiums, even though they are not explicitly required to do so by statute. Communities in high-density markets like Greater Boston, the North Shore, and the South Shore increasingly treat professional reserve studies as standard operating procedure, regardless of legal mandate.

What Chapter 183A actually requires for condos

Chapter 183A is the Massachusetts Condominium Act, and it is the primary statute governing condominium governance and finances across the Commonwealth. Several sections are directly relevant to reserve planning.

Section 10(i) — the reserve fund mandate. Section 10(i) states plainly that "all condominiums shall be required to maintain an adequate replacement reserve fund, collected as part of the common expenses and deposited in an account or accounts separate and segregated from operating funds." This applies to every condominium association in Massachusetts, from a six-unit converted triple-decker in Lowell to a 200-unit high-rise in downtown Boston.

Section 1 — definition of replacement reserve fund. Section 1 of Chapter 183A defines "replacement reserve fund" as a separate and segregated portion of the common funds of the organization of unit owners, used to replace, restore, or rebuild common areas and facilities and certain limited common areas for which the organization is responsible.

Section 10(f) — managing agent quarterly reporting. Under Section 183A-10(f), managing agents are required to render written reports to the trustees at least quarterly. These reports must include beginning and ending balances, copies of all relevant bank statements, and reconciliations for the replacement reserve fund. The reserve account must be maintained as a separate and distinct account. This provision ensures transparency and gives trustees a regular check on whether reserve funds are being properly collected and held. Boards that self-manage should adopt this same quarterly reporting discipline voluntarily.

The statute does not specify:

- a minimum percentage of the operating budget that must be contributed to reserves;

- a required dollar amount per unit; or

- a mandatory schedule for reviewing reserve adequacy.

Instead, it leaves "adequate" to be interpreted in context. Massachusetts condominium law firms and commentators consistently advise that trustees must take the requirement seriously, treat reserves as a core fiduciary duty, and keep funds in a genuinely separate account rather than co-mingled with operating funds.

It is also worth noting that some Massachusetts condominiums are organized as trusts rather than traditional associations. Condominium trusts operate under slightly different governance structures, but the Chapter 183A reserve fund requirements apply equally. Trustees of a condominium trust have the same fiduciary obligations to unit owners regarding reserve fund adequacy and segregation.

Reserve study requirements: current status and proposed changes

Because of tragedies like the Surfside condominium collapse and tightening standards in states such as Florida and Hawaii, many Massachusetts boards assume similar reserve study mandates already exist in the Commonwealth. They do not, at least not yet. CAI's multi-state summary and multiple reserve study providers list Massachusetts as a state where reserve funding is required for condos, but reserve studies are not legally mandated.

There have been periodic legislative proposals, such as past Senate Bill 980, which would have required capital reserve fund studies for larger condominium associations, but these have not been enacted as of early 2026.

For now, "Massachusetts reserve study requirements" are best understood as best practices and lender expectations, not statutory mandates. However, the trend nationally is toward more regulation, not less.

Boards that implement regular reserve studies now will be better positioned if Massachusetts eventually codifies study requirements, and they will be more defensible if challenged by owners about financial planning.

How much does a reserve study cost in Massachusetts?

A professional reserve study in Massachusetts typically costs between $2,500 and $10,000, depending on several factors. For a nationwide breakdown of how much reserve studies cost, see our comprehensive cost guide. Key factors include:

- Community size. A small 20-unit townhome community will cost significantly less than a 150-unit condominium complex with multiple buildings, a parking garage, and extensive common areas.

- Number of components. More common-area components (roofs, boilers, elevators, pools, paved surfaces, building envelope elements) means more inspection time and more line items in the funding analysis.

- Building complexity. Historic conversions, mixed-use properties, and high-rise buildings with mechanical systems, elevators, and underground parking require more specialized assessment than standard garden-style communities.

- Study level. A Level 1 full reserve study with on-site inspection costs more than a Level 3 update without a site visit. Most Massachusetts communities should start with a Level 1 study and follow up with Level 2 or 3 updates in subsequent cycles.

Greater Boston properties tend toward the higher end of the cost range, reflecting the area's elevated labor rates and the complexity of urban condominium buildings. Communities in suburban and western Massachusetts, such as those in Springfield, Worcester, or the Pioneer Valley, typically fall in the lower-to-mid range.

The cost of a reserve study is modest compared to the cost of a single poorly planned special assessment. A $5,000 study that prevents a $200,000 surprise assessment is one of the highest-return investments a board can make.

New England climate factors and reserve planning

Massachusetts communities face building deterioration challenges that are significantly more severe than national averages. The New England climate is one of the harshest in the country for building components, and reserve studies for Massachusetts properties must account for these accelerated deterioration rates.

Freeze-thaw cycles. Massachusetts experiences dozens of freeze-thaw cycles each winter. Water infiltrates concrete, masonry, and asphalt, then expands as it freezes. Over years, this causes concrete spalling on balconies and parking structures, pavement heaving and cracking in driveways and walkways, mortar joint deterioration in brick facades, and foundation cracking in older buildings. Components that might last 25 years in a temperate climate may need replacement in 15 to 20 years in Massachusetts.

Ice dams and roof damage. Heavy snowfall combined with heat loss through poorly insulated roofs creates ice dams, which force water under shingles and into the building envelope. Ice dam damage is one of the most common and costly repair items for Massachusetts condominium associations, particularly in older buildings with inadequate insulation. Reserve studies must account for shorter roof lifespans and the likelihood of periodic ice dam repair costs between full replacements.

Salt damage to parking structures and pavement. Road salt and de-icing chemicals are essential for safety but corrosive to concrete, rebar, and asphalt. Parking garages and surface lots in Massachusetts deteriorate faster than in states where salt use is minimal. Communities in Boston, Cambridge, Quincy, and other urban areas with structured parking should budget for accelerated concrete repair and sealant cycles.

Boiler and heating system lifecycle. New England's long heating season puts extraordinary demand on boilers, furnaces, and heating distribution systems. A commercial boiler serving a Massachusetts condominium complex typically runs six to seven months per year at high output. This shortens equipment lifespan compared to properties in milder climates, and boiler replacement is one of the highest single-cost reserve items for Massachusetts communities. Depending on size and fuel type, a commercial boiler replacement can range from $50,000 to $200,000 or more.

Building envelope stress. The combination of wind-driven rain, freeze-thaw, ice, and temperature extremes puts severe stress on siding, windows, doors, and exterior trim. Exterior paint failure is accelerated, caulking and sealants degrade faster, and window replacement cycles are shorter. Massachusetts communities, particularly those along the coast from Cape Cod to the North Shore, face additional exposure to salt air and storm surge.

Common Massachusetts-specific reserve components. Beyond standard reserve items, Massachusetts communities should ensure their reserve studies include: boilers and heating distribution systems, ice and snow removal equipment, building envelope elements (siding, windows, exterior trim), parking structure maintenance and concrete repair, elevator modernization (in larger Boston-area properties), and storm drainage systems designed for heavy New England precipitation.

A reserve study that uses national-average component lifespans will systematically underestimate the reserve needs of a Massachusetts community. Boards should insist that their reserve study professional applies New England-adjusted lifespans and Massachusetts-specific replacement costs.

How much should Massachusetts associations keep in reserves?

Because the law does not assign a percentage, boards often ask for a simple rule of thumb for reserve funding. Many New England reserve professionals and articles aimed at Massachusetts associations suggest:

- using a professional reserve study to estimate long-term capital needs;

- avoiding reliance on a flat "10% of budget" rule unless it has been confirmed by a study; and

- targeting funding levels that keep the community out of crisis, meaning reserves are sufficient to handle predictable major projects without constant large special assessments.

The popular "10 to 20 percent of budget" guideline is only a starting point. A small two-building garden-style condo in Brockton with minimal amenities might need less; a large high-rise in downtown Boston with elevators, a parking garage, and complex mechanical systems might need much more. Adequacy depends on components, age, climate exposure, and risk tolerance — exactly the factors a reserve study is designed to quantify. Understanding what fully funded reserves mean can help boards set meaningful targets beyond simple percentage rules.

Massachusetts associations can also amend their bylaws to require reserve contributions when units change hands. This is a mechanism some communities use to boost reserve funding at the point of sale, ensuring that buyers contribute to the reserves for the building they are entering. While not common statewide, it is a tool available under Massachusetts law and worth considering for underfunded communities.

Lender requirements: the de facto reserve study mandate

Even though Massachusetts law does not require reserve studies, federal lending guidelines create a practical mandate that affects every community where unit owners need mortgages.

FHA requirements. The Federal Housing Administration requires that condominium projects seeking FHA approval demonstrate that at least 10 percent of the annual operating budget is allocated to a replacement reserve fund, or that a current reserve study shows the reserves are adequately funded. Without FHA approval, buyers cannot use FHA-insured loans to purchase units in the community, which significantly limits the buyer pool and can depress property values.

Fannie Mae and Freddie Mac requirements. Conventional mortgage lenders backed by Fannie Mae and Freddie Mac apply similar standards. A condominium project that cannot demonstrate adequate reserves, either through the 10 percent benchmark or a current reserve study, may be classified as "non-warrantable." Non-warrantable condominiums face severely restricted financing options: fewer lenders will offer mortgages, and those that do typically charge higher rates and require larger down payments.

The practical impact. For Massachusetts condominium associations, these lending requirements mean that failing to maintain adequate reserves or failing to have a current reserve study can directly harm unit owners' ability to sell or refinance. In competitive markets like Greater Boston, Cambridge, and Quincy, where property values are high and buyers rely heavily on financing, the lending requirement effectively makes reserve studies mandatory for any community that wants to maintain its marketability.

Boards should view the 10 percent rule not as a ceiling but as a minimum floor. A professional reserve study almost always reveals that 10 percent of the operating budget is insufficient for older buildings with complex systems, which describes a large share of the Massachusetts condominium market.

Are reserve studies necessary if they are not required?

Legally, you can be a Massachusetts condo trustee with no reserve study on file and still be in technical compliance with Chapter 183A if your reserve fund is somehow "adequate." Practically, that position is difficult to defend.

Without a study, trustees are making judgment calls on:

- expected remaining useful lives of roofs, boilers, siding, windows, and pavement;

- realistic replacement costs in a high-inflation, high-construction-cost environment; and

- how to spread contributions fairly among current and future owners.

Massachusetts-focused guidance from industry and legal sources repeatedly recommends reserve studies as the best way to show that trustees exercised informed judgment. This is particularly important in Massachusetts, where the aging building stock, harsh climate, and elevated construction costs make accurate projections especially challenging without professional analysis. Deferred maintenance in New England compounds quickly — what starts as a minor envelope issue can become a six-figure structural repair within a few years.

In the event of a dispute, for example after a large special assessment or a major building failure, having a professional reserve study and evidence that the board followed it is far more defensible than relying on informal estimates.

Recommended frequency for reserve studies in Massachusetts

With no statutory cadence, the industry standard fills the gap. Most experts recommend:

- a full reserve study with site visit every three to five years; and

- internal review and minor updates annually as part of the budget process.

For newer communities with straightforward components and strong initial funding, a five-year cycle may be adequate. Older buildings, complexes with significant structural or mechanical systems, or associations that are clearly underfunded benefit from more frequent reviews. Communities in harsh-climate zones, including coastal properties on Cape Cod, the North Shore, and the South Shore, may want to lean toward the three-year end of the range because of accelerated component deterioration.

For HOAs, this cycle is just as relevant. Even though there is no Chapter 183A equivalent for HOAs, roads, clubhouses, pools, and stormwater systems still age. Reserve studies help HOA boards show they are fulfilling their fiduciary duty and can support long-term capital planning even without a specific statute.

After severe weather events, such as a major nor'easter, ice storm, or flooding, boards should consider commissioning an interim update to re-baseline component conditions and projected costs. For guidance on how to read and use your reserve study once complete, see our detailed walkthrough.

Practical roadmap for Massachusetts boards

A practical, non-disruptive approach for Massachusetts associations that want to solidify their position:

Step 1: Confirm your structure and obligations

If you are a condominium, Chapter 183A applies and you must maintain an adequate replacement reserve fund in a segregated account. If your condominium is organized as a trust, the same requirements apply. If you are a non-condo HOA, review your declaration and bylaws for any reserve obligations.

Step 2: Assess your current reserves

Compare your current reserve balance and annual contributions against upcoming major projects, including roofs, paving, siding, boilers, and mechanical systems. If upcoming needs significantly outstrip reserves, adequacy is doubtful. Pay particular attention to components affected by New England climate stress.

Step 3: Commission or update a professional reserve study

Even though it is not mandated, a study from a qualified reserve study professional gives you a defensible basis for contribution decisions and helps you explain funding needs to owners. Ensure the professional applies Massachusetts-specific cost data and climate-adjusted component lifespans. Our reserve study preparation checklist can help your board gather the right documents before the engagement begins.

Step 4: Review lender compliance

Verify that your reserve funding meets the 10 percent threshold required by FHA and conventional lenders, or that you have a current reserve study demonstrating adequate funding. This protects your owners' ability to sell and refinance.

Step 5: Build a funding plan that owners can understand

Use the study to move gradually toward adequate funding, rather than trying to fix everything in one budget year. The goal is to avoid both chronic underfunding and shock assessments. If your community is significantly underfunded, consider phasing increases over three to five years. Our guide to recovery plans for underfunded HOAs walks through practical strategies for closing the gap without shocking owners.

Step 6: Communicate clearly

Explain Chapter 183A's reserve requirement, share key findings from the reserve study, and show how the funding plan protects both the buildings and property values. Massachusetts owners are far more likely to accept increases when they understand the legal and practical reasons behind them. Transparency about the managing agent's quarterly reports builds additional trust.

Ready to get started? Request your reserve study from PropFusion — our team delivers professional studies tailored to New England building conditions and Chapter 183A compliance.

Related resources

- Reserve Study Services in Massachusetts

- Reserve Study Requirements by State

- HOA Reserve Study: Everything You Need to Know

- Three Types of Reserve Fund Studies (Level I–III)

- New York Reserve Study Requirements

- Connecticut Reserve Study Requirements

- New Hampshire Reserve Study Requirements

- Rhode Island Reserve Study Requirements

- Vermont Reserve Study Requirements

- Maine Reserve Study Requirements

Related reserve study resources for Massachusetts

Compare reserve study laws in nearby states, or find help running one for your association:

Frequently asked questions

Are reserve studies mandatory for Massachusetts condominiums?

No. Massachusetts does not currently mandate reserve studies for condominiums. What it does mandate is that all condominiums maintain an adequate replacement reserve fund in a segregated account under Chapter 183A, Section 10(i). A reserve study is the most practical way to determine whether that fund is adequate, but it is not required by statute.

Do Massachusetts HOA reserve fund laws require specific contribution percentages?

No. There is no statute that sets a minimum reserve contribution percentage for HOAs or condos, such as "10% of the budget." Contribution levels are determined by expected component costs and lifecycles, the association's governing documents, and the board's judgment, typically guided by a professional reserve study.

What happens if a Massachusetts condo has little or no reserve fund?

A condo that fails to maintain an adequate replacement reserve fund is out of step with Chapter 183A and exposes trustees to risk, particularly if major repairs become necessary and there is no money set aside. In practice, this often leads to large special assessments, deferred maintenance, or the need for loans — all of which can harm property values and owner trust. Communities in this position also risk being classified as non-warrantable by lenders, which restricts buyers' ability to obtain financing.

How often should Massachusetts boards update their reserve study?

Industry best practice for Massachusetts is to obtain a full reserve study every three to five years, with annual reviews tied to the budgeting process. Older buildings, underfunded communities, or properties with complex systems may benefit from more frequent updates, even though the law does not specify a frequency. Communities exposed to severe New England weather should lean toward the three-year cycle.

Are HOAs in Massachusetts safer ignoring reserves because there is no statute?

No. The absence of a specific HOA reserve statute does not eliminate board fiduciary duties. Roads, stormwater systems, amenities, and other HOA common assets still wear out. Ignoring reserves typically results in emergency special assessments, conflict with owners, and potential claims that the board failed to plan responsibly. A reserve study and funding plan are still strongly recommended.

How can PropFusion help our Massachusetts community?

PropFusion produces reserve studies for Massachusetts communities, from small townhome conversions to large high-rise complexes. Our team handles the full process — site inspection, component inventory, 30-year funding analysis, and final report — using New England-adjusted lifespans and Massachusetts-specific cost data. That combination helps boards meet Chapter 183A obligations, demonstrate responsible planning, and maintain stable fees over time.

How much does a reserve study cost in Massachusetts?

A professional reserve study in Massachusetts typically costs between $2,500 and $10,000. The primary cost factors are community size, number of common-area components, building complexity, and study level. Greater Boston properties generally fall at the higher end of the range due to the area's elevated labor costs and the complexity of urban condominium buildings, while suburban and western Massachusetts communities typically fall in the lower-to-mid range. A Level 1 full study with on-site inspection costs more than a Level 2 or Level 3 update.

How does New England's climate affect reserve study planning?

New England's harsh climate significantly impacts reserve planning for Massachusetts communities. Dozens of freeze-thaw cycles each winter cause concrete spalling, pavement heaving, and masonry deterioration. Ice dams damage roofs and building envelopes, salt and de-icing chemicals corrode parking structures, and long heating seasons shorten boiler lifespans. Components that last 25 years in temperate climates may need replacement in 15 to 20 years in Massachusetts. A properly conducted reserve study should use New England-adjusted component lifespans and Massachusetts-specific replacement costs rather than national averages.

Do FHA or Fannie Mae require reserve studies for Massachusetts condos?

Not directly, but the practical effect is similar. FHA requires condominium projects to allocate at least 10 percent of the annual operating budget to a replacement reserve fund, or to have a current reserve study demonstrating adequate funding, in order to be eligible for FHA-insured mortgages. Fannie Mae and Freddie Mac apply similar standards for conventional loans. A condominium project that fails these benchmarks may be classified as non-warrantable, severely limiting buyers' financing options and potentially reducing property values. For Massachusetts communities where owners depend on mortgage financing, these requirements make reserve studies practically essential.

The information contained on this page is provided for informational purposes only, and should not be construed as legal advice on any subject matter. You should not act or refrain from acting on the basis of any content included on this page without seeking legal or other professional advice. The contents of this page contain general information and may not reflect current legal developments or address your situation. We disclaim all liability for actions you take or fail to take based on any content on this report.

PropFusion delivers professional reserve studies with 30-year funding plans - powered by modern technology and backed by certified reserve analysts.

Take the guesswork out of your reserve study

From site inspection to 30-year funding plan, PropFusion handles the entire reserve study - accurate, transparent, and built on modern technology that gives you full control over your reserves.