New York Reserve Study Requirements (2026)

New York does not require every HOA, condominium, or co-op to perform a formal reserve study. Instead, reserve obligations come from a patchwork of Real Property Law provisions, Business Corporation Law fiduciary duties, NYC conversion rules, and lender requirements that function as de facto mandates.

This guide covers what New York law requires today, how proposed bills S7600 and A8945 would change the landscape, and how boards can use reserve studies to satisfy fiduciary duties and protect property values.

Legislation Links

NY Real Property Law §339-V (Condo Bylaws)

NY Senate Bill S7600 (Proposed Reserve Study Mandate)

NY Assembly Bill A8945 (Companion to S7600)

Does New York law require reserve studies? No statewide statute mandates reserve studies for all HOAs, condos, or co-ops. However, Fannie Mae requires condos to allocate at least 10% of their operating budget to reserves for conventional mortgage eligibility. Buildings that fail this threshold become "non-warrantable," blocking owners from obtaining conventional financing.

What are bills S7600 and A8945? These proposed bills would require condos and co-ops to complete capital reserve studies with 30-year funding plans, prepared by credentialed professionals, and filed with the Attorney General. S7600 has been reported out of committee but has not yet become law.

How does the Business Judgment Rule relate to reserve planning? Under the BJR established in Levandusky v. One Fifth Avenue (1990), courts defer to board decisions made in good faith and on an informed basis. A board that commissions a professional reserve study has a strong BJR defense. A board that sets contributions without professional analysis is vulnerable to liability claims.

PropFusion delivers professional reserve studies with 30-year funding plans - powered by modern technology and backed by certified reserve analysts.

New York Reserve Study Requirements: What the Law Says

New York is one of the few major states without a single statute requiring every community association to conduct a reserve study. Instead, New York reserve study requirements emerge from overlapping sources — condominium bylaws under Real Property Law, co-op fiduciary duties under the Business Corporation Law, NYC conversion rules, and federal lending standards.

Condominium Act Framework

Real Property Law §339-V establishes what condo bylaws must and may address, including provisions for "reserves" covering major and minor maintenance, repairs, improvements, and working capital. The statute allows but does not compel a specific reserve level or study schedule.

Each condominium's board of managers sets reserve policy within the boundaries of its declaration and bylaws. For a deeper understanding of how reserve studies fit into condo governance, see our guide on who performs reserve studies.

Co-op Reserve Expectations

New York cooperative corporations are governed by the Business Corporation Law, which requires directors to act in good faith and with the degree of care an ordinarily prudent person would use. While the BCL does not use the term "reserve study," related guidance requires co-op boards to periodically set aside reasonable sums for reserves.

For co-ops with underlying mortgages — the vast majority of NYC co-ops — the lender holding the building's mortgage often imposes its own reserve requirements as a loan covenant. Boards should review their recognition agreements carefully.

NYC Conversion Reserve Funds

For certain affordable-housing preservation conversions in New York City, Real Property Law §339-MM and NYC Administrative Code §26-703 require the sponsor to establish a condominium reserve fund and a dedicated capital fund within 30 days of the preservation plan's consummation. These provisions include contribution formulas, mandatory annual reporting, and civil penalties for noncompliance.

Planned Communities and HOAs

Many New York HOAs are organized under not-for-profit corporation statutes or as condominiums. Their governing documents — not a special HOA statute — define reserve contributions. Boards follow the same reserve study best practices as condos because buyers, lenders, and insurers assess financial health in similar ways.

Condos vs. Co-ops vs. HOAs: New York Reserve Rules Compared

| Feature | Condominiums | Co-ops | HOAs / Planned Communities |

|---|---|---|---|

| Governing Law | Real Property Law §339 | Business Corporation Law | N-PCL or Condo Act |

| Reserve Study Required? | No statewide mandate | No statewide mandate | No statewide mandate |

| Reserve Fund Required? | Per bylaws (typically yes) | Fiduciary duty to maintain | Per governing documents |

| Fannie Mae 10% Rule | Yes — affects warrantability | N/A (different lending structure) | Yes — affects warrantability |

| Proposed Legislation | S7600/A8945 would mandate | S7600/A8945 would mandate | Not currently included |

| Unique Funding Source | Common charges | Maintenance fees + flip tax | Assessments |

| Lender Reserve Covenants | Fannie Mae / Freddie Mac | Underlying mortgage lender | Fannie Mae / Freddie Mac |

| FISP / Local Law 11 | Yes (6+ stories in NYC) | Yes (6+ stories in NYC) | Rarely applies |

Proposed Reserve Study Mandates: S7600 and A8945

Bills S7600 and A8945, introduced in the 2025-2026 legislative session, would materially change reserve study obligations in New York. Both bills would require condominium and cooperative associations to complete capital reserve studies that:

- Include a 30-year funding plan

- Analyze capital components, their condition, useful lives, and replacement costs

- Review reserve fund balances, anticipated income and expenses, and the costs of future studies and corrective work

- Are prepared or overseen by a credentialed reserve specialist, architect, or engineer

The bills also contemplate timelines for catching up underfunded reserves and ongoing board review of studies, with studies filed with the Attorney General. As of the latest published actions, S7600 has been reported out of committee but has not been adopted into law.

For your board, this means two things. Do not assume these obligations are in force yet — verify current status with counsel. But designing your reserve study and funding plan around these standards now is a smart way to future-proof your community.

Are Reserve Studies Required in New York Today?

For most HOAs, condos, and co-ops, the answer is no, not by statewide statute. CAI's national summary and multiple legal sources confirm that New York does not impose a statutory requirement to perform reserve studies or fund reserves at a specific level for all associations, outside of the special NYC conversion rules noted above.

However, boards can still be effectively forced into reserve planning by three factors:

- Governing documents that require reserve budgets, long-term capital plans, or periodic engineering reports

- Lender guidelines — Fannie Mae requires condos to maintain reserves of at least 10% of the operating budget for warrantability, directly affecting buyers' ability to get financing

- Fiduciary duties — failing to plan for predictable capital projects can lead to large special assessments and claims that the board breached its duty of care

Even without a statutory mandate, New York boards that ignore reserve studies do so at their peril. For guidance on adequate reserve levels, see our explainer on what fully funded reserves mean.

The Business Judgment Rule and Reserve Planning

The Business Judgment Rule (BJR) is one of the most important legal doctrines governing New York condo and co-op boards. Under the BJR, as articulated in Levandusky v. One Fifth Avenue Apartment Corp. (1990), courts defer to board decisions made in good faith, within authority, and on a reasonably informed basis.

A board that commissions a professional reserve study, reviews its findings, and adopts a funding plan based on expert analysis has a strong BJR defense if owners later challenge assessment levels or capital project timing. The board acted on expert advice — the decision was informed.

Conversely, a board that sets reserve contributions without professional analysis — relying on guesswork or a desire to keep fees low — is vulnerable to challenge. As the Appellate Division noted in Pomerance v. McGrath (2013), courts examine whether the board undertook a reasonable investigation before making its decision.

For co-ops, the BJR analysis is even more critical. Co-op boards that fail to plan for capital expenditures risk impairment of underlying mortgage terms, share values, and shareholders' ability to obtain recognition agreements. A reserve study is the single most cost-effective step a New York board can take to demonstrate informed decision-making.

Fannie Mae, Freddie Mac, and De Facto Reserve Requirements

While Albany has not passed a reserve study mandate, Fannie Mae and Freddie Mac have imposed requirements that function as one. Under current guidelines, a condominium must allocate at least 10% of its total annual operating budget to replacement reserves to be considered "warrantable."

What Happens When a Building Fails the 10% Threshold

The building becomes "non-warrantable." This means no lender will issue a conventional mortgage for any unit in the building. In New York City, where median apartment prices in Manhattan exceed $1 million, non-warrantable status can:

- Prevent unit owners from selling to buyers who need a mortgage

- Block owners from refinancing existing loans

- Depress property values across the entire building

- Force buyers to seek portfolio loans with higher rates and larger down payments

A professional reserve study is the most direct way for a New York condo board to demonstrate compliance with the 10% threshold and document that deferred maintenance is being addressed.

For FHA-insured loans, the requirements are even more explicit — FHA project approval often requires evidence of adequate reserves and a current reserve study. Buildings seeking or maintaining FHA certification should treat reserve studies as a prerequisite.

NYC Condo Budget Timeline and Reserve Requirements

New York City condos and co-ops face a unique budget timeline that directly intersects with reserve planning. Understanding these deadlines helps boards align their reserve study schedule with annual budget cycles and lender reporting requirements.

Annual Budget Cycle

Most NYC condo boards adopt annual budgets between October and December for the following calendar year. Reserve study findings should be available before the budget cycle begins so that recommended contribution levels can be incorporated into the annual budget.

Lender Questionnaire Deadlines

Fannie Mae and Freddie Mac require responses to project eligibility questionnaires before approving mortgages in a building. These questionnaires ask specifically about the 10% reserve allocation, deferred maintenance, and special assessments. Boards should maintain current reserve study data to respond promptly.

Recommended Timeline

- Q1: Review prior year's reserve fund performance against the study's projections

- Q2–Q3: Commission or update the reserve study (coordinate with any FISP inspections)

- Q4: Incorporate reserve study recommendations into the annual budget

- Ongoing: Maintain documentation for lender questionnaires

Aligning your reserve study with the budget timeline ensures that contribution increases are planned, not reactive. For boards preparing for their first study, see our reserve study preparation checklist.

Local Law 11 (FISP) and Reserve Study Coordination

For NYC buildings six stories or taller, Local Law 11 — now the Facade Inspection and Safety Program (FISP) — requires critical examination of exterior walls by a Qualified Exterior Wall Inspector (QEWI) every five years. The current inspection cycle (Cycle 9) runs through 2027.

FISP findings have major implications for reserve planning because facade repair is one of the single largest capital expenditure categories for NYC buildings. Scaffolding, waterproofing, brick repointing, and window replacement can cost hundreds of thousands to millions of dollars.

How FISP and Reserve Studies Work Together

- FISP findings inform reserve component costs. Conditions identified by the QEWI should be incorporated into the reserve study's component inventory.

- Reserve studies anticipate the next FISP cycle. Project facade-related expenditures across multiple 5-year cycles, not just the current one.

- Timing coordination. Schedule reserve study updates to follow FISP inspections so the most current facade data is reflected.

FISP does not replace the need for a reserve study. FISP addresses only exterior walls and appurtenances, while a reserve study covers the full range of common-area components — roofs, elevators, boilers, plumbing, lobbies, parking structures, and amenity spaces.

How Much Does a Reserve Study Cost in New York?

Reserve study costs in New York vary significantly by geography, building type, and complexity. For a nationwide breakdown, see our reserve study cost guide.

New York City (Five Boroughs)

For NYC condos, co-ops, and high-rise buildings, reserve studies typically cost $10,000 to $40,000. This premium reflects high labor costs, complex building systems (elevators, boilers, cooling towers, FISP-regulated facades), building height, access logistics, and the frequent requirement for a PE-licensed professional.

Suburban New York (Westchester, Long Island)

For suburban communities, townhome associations, and mid-rise buildings outside the five boroughs, costs typically range from $5,000 to $15,000.

Upstate New York (Albany, Syracuse, Rochester, Buffalo)

For upstate communities with lower labor costs and smaller buildings, reserve studies generally range from $3,000 to $10,000.

Across all regions, cost depends on study level. Our overview of the three types of reserve fund studies explains what Level I, II, and III studies cover.

How Often Should New York Boards Commission Reserve Studies?

Even without a statutory clock, reserve studies lose usefulness as costs, inflation, and building conditions change. Most New York associations should follow this schedule:

- Baseline (Level I) study: When a building is new, after a major renovation, or when the board realizes there is no current long-term plan

- Updates every 3-5 years: To keep component inventories, remaining useful lives, and cost estimates current

- Interim updates sooner if: Significant capital projects are completed early or late, inflation moves sharply, the association falls behind its recommended funding trajectory, or a new FISP report reveals unexpected conditions

For buildings likely to fall under S7600/A8945, aligning your update cycle with a 30-year forecast and annual board review mirrors the proposed bill language. For guidance on how to read and use your reserve study, see our detailed walkthrough.

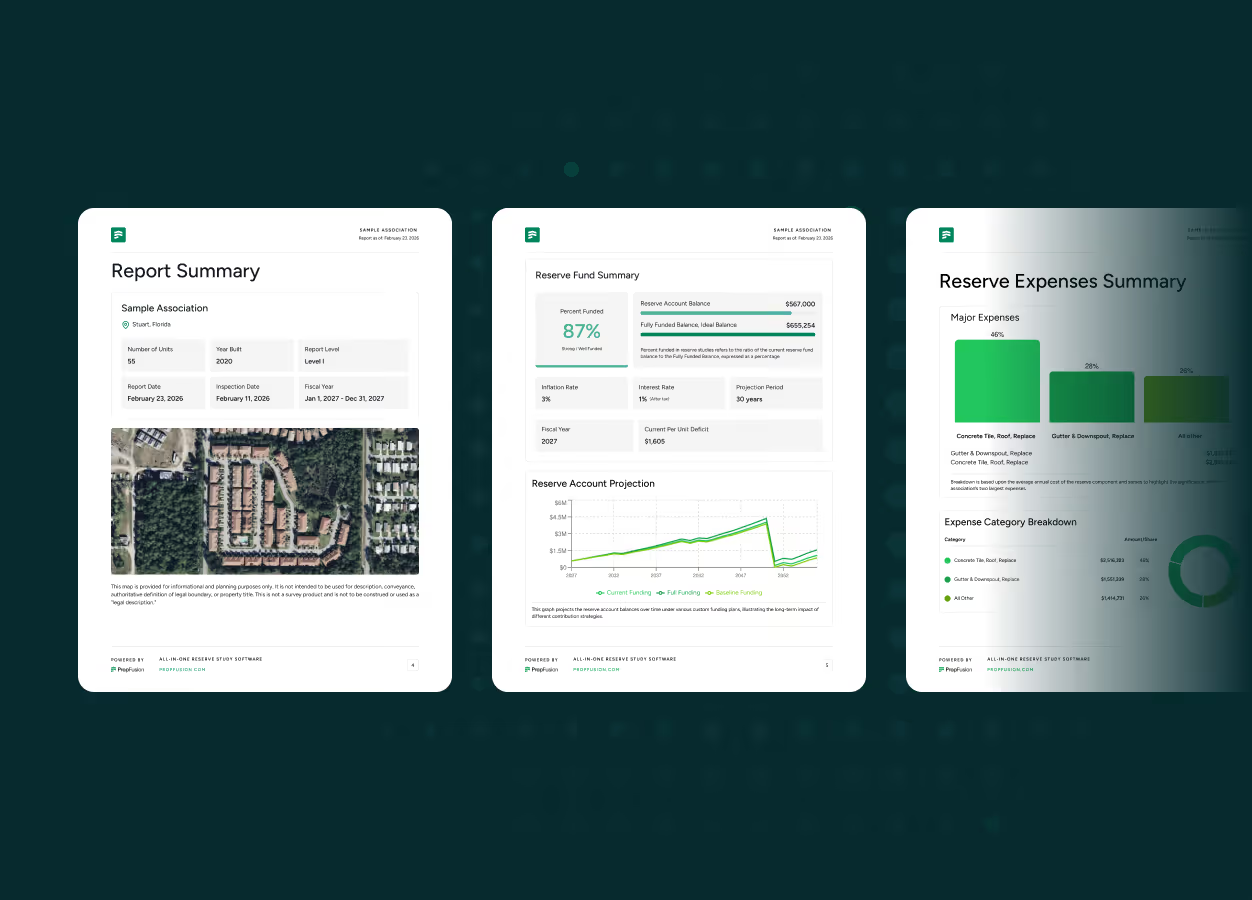

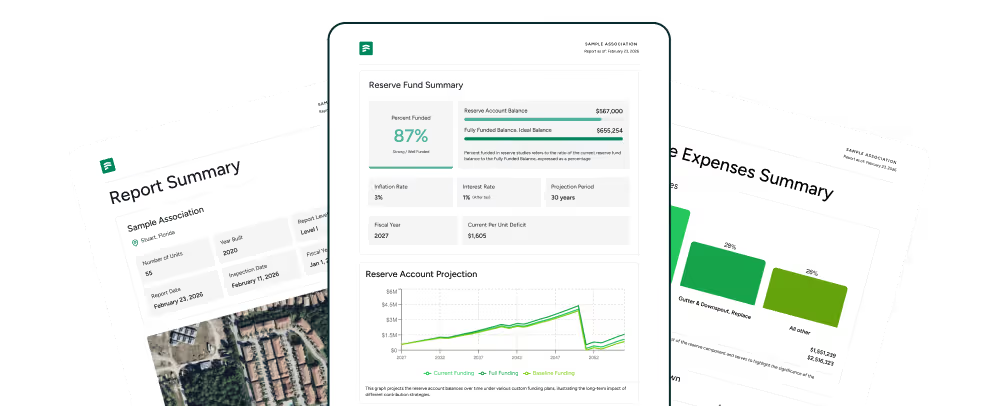

What a New York Reserve Study Should Include

A high-quality reserve study for a New York community should include:

- Physical analysis of all common elements: roofs, facades and FISP-regulated assemblies, elevators, boilers, chillers, cooling towers, garages, lobbies, corridors, windows, amenity spaces, fire suppression systems, and site components

- Condition assessment and remaining useful life estimates for each component

- Current replacement cost estimates and inflation assumptions tailored to the New York market

- Documentation of current reserve fund balance, anticipated income (contributions, special assessments, flip tax revenue for co-ops), and projected capital outflows by year

- A 20- to 30-year funding plan showing annual contributions necessary to avoid reserve deficits

- Compliance analysis addressing the Fannie Mae 10% threshold and any lender or mortgage covenants

- Percent funded analysis — the ratio of the reserve fund's actual balance to its fully funded balance

Industry benchmarks classify reserve funding levels as: above 70% is strong, 30-70% is fair but may need increases, and below 30% is weak with significant special assessment risk. For boards unfamiliar with this concept, see our explainer on what fully funded reserves mean.

Practical Steps for New York Boards

Step 1: Confirm Your Legal Baseline

Review your declaration, bylaws, proprietary lease (co-ops), and existing engineering reports to determine if reserve studies or funding levels are already required internally. For co-ops, review underlying mortgage documents for reserve fund covenants.

Step 2: Commission or Update a Reserve Study

Engage a New York-experienced reserve professional. Provide prior studies, financial statements, capital project histories, and any FISP reports. Ensure the study scope covers all common-area components. For guidance on preparing for your reserve study, see our preparation checklist.

Step 3: Adopt a Funding Plan

Use the study's recommended contribution range as your starting point. Verify the plan keeps contributions at or above the Fannie Mae 10% threshold and avoids shortfalls within 10-20 years. Aim for at least 70% funded status. Understanding different reserve funding methods helps boards select the right approach for their community.

Step 4: Communicate with Owners

Share key graphs and funding scenarios with owners before adopting the budget. Explain how the plan reduces surprise assessments and protects property values. If your community faces a shortfall, see our guide on recovery plans for underfunded reserves.

Step 5: Monitor Legislation

Have your managing agent or counsel track S7600, A8945, and any successor bills. If they pass, map your existing study against the statutory requirements and update where needed.

Ready to take the first step? Request a reserve study proposal from PropFusion — we deliver professional reserve studies for New York condos, co-ops, and HOAs statewide.

Related Resources

- Reserve Study Requirements by State

- How Much Do HOA Reserve Studies Cost?

- Three Types of Reserve Fund Studies

- What Does Fully Funded Reserves Mean?

- New Jersey Reserve Study Requirements

- Connecticut Reserve Study Requirements

- Pennsylvania Reserve Study Requirements

Related reserve study resources for New York

Compare reserve study laws in nearby states, or find help running one for your association:

Frequently Asked Questions

Does New York law require every HOA or condo to have a reserve fund?

No. Outside of specific NYC conversion situations governed by Real Property Law §339-MM, New York does not impose a universal reserve fund requirement. Most communities rely on their bylaws, lender expectations (particularly the Fannie Mae 10% threshold), and professional reserve studies to determine appropriate funding levels.

Are reserve studies mandatory for co-ops in New York?

Co-ops are expected to set aside "reasonable" reserves under New York's cooperative corporation framework, but there is no explicit statutory requirement for formal reserve studies on a set schedule. In practice, many co-op boards use reserve studies to demonstrate adequate reserves, satisfy underlying mortgage covenants, and build a strong Business Judgment Rule defense.

How will S7600 and A8945 affect my condo or co-op if they pass?

If enacted, these bills would require condos and co-ops to complete capital reserve studies with 30-year funding plans, have them prepared by qualified professionals, review them annually, and file them with the Attorney General. Boards should plan as if these standards will apply but confirm current legislative status with counsel.

What is a "non-warrantable" building and how does it relate to reserves?

A non-warrantable building fails to meet Fannie Mae or Freddie Mac eligibility requirements for conventional mortgages. One of the most common reasons is insufficient reserve funding — failing to allocate at least 10% of the operating budget to replacement reserves. When classified as non-warrantable, no unit owner can obtain a conventional mortgage, limiting buyers to higher-rate portfolio loans and depressing property values.

How much does a reserve study cost in New York City?

Reserve study costs in NYC range from $10,000 to $40,000 depending on building height, unit count, and system complexity. Suburban communities (Westchester, Long Island) typically pay $5,000 to $15,000, while upstate communities pay $3,000 to $10,000.

Does Local Law 11 (FISP) replace the need for a reserve study?

No. FISP requires exterior wall inspections every five years for buildings six stories or taller, but it addresses only facades. A reserve study covers the full range of common-area components — roofs, elevators, boilers, plumbing, lobbies, and more. The two are complementary: FISP findings should feed into reserve study projections, but FISP alone does not provide the funding plan or financial analysis a reserve study delivers.

What reserve funding level is considered "healthy" in New York?

Reserve professionals generally use three benchmarks: above 70% funded is strong, 30-70% is fair but may require contribution increases, and below 30% is weak with high special assessment risk. Separately, Fannie Mae requires at least 10% of the operating budget to be allocated to reserves for warrantability.

How often should we update our reserve study?

Industry best practice is every 3-5 years, with interim financial updates in off years. If your building undergoes a major FISP inspection, experiences significant cost changes, or falls behind on its funding plan, update sooner.

Can we waive reserve fund contributions in New York?

Some governing documents permit owners to vote to reduce contributions, but doing so increases special assessment risk, may conflict with lender requirements, and could jeopardize Fannie Mae warrantability. Co-op boards should also check whether underlying mortgage covenants restrict changes to reserve funding. Obtain legal advice before cutting reserve funding.

Are there special reserve rules for NYC condo conversions?

Yes. Certain conversions tied to affordable-housing preservation must fund specific reserve and capital accounts under Real Property Law §339-MM and NYC Administrative Code §26-703. These include contribution formulas tied to percentages of total price and civil penalties for noncompliance.

The information contained on this page is provided for informational purposes only, and should not be construed as legal advice on any subject matter. You should not act or refrain from acting on the basis of any content included on this page without seeking legal or other professional advice. The contents of this page contain general information and may not reflect current legal developments or address your situation. We disclaim all liability for actions you take or fail to take based on any content on this report.

PropFusion delivers professional reserve studies with 30-year funding plans - powered by modern technology and backed by certified reserve analysts.

Take the guesswork out of your reserve study

From site inspection to 30-year funding plan, PropFusion handles the entire reserve study - accurate, transparent, and built on modern technology that gives you full control over your reserves.