How Underfunded New Jersey Associations Can Catch Up Over 10 Years

PropFusion delivers professional reserve studies with 30-year funding plans - powered by modern technology and backed by certified reserve analysts.

Why so many New Jersey associations are behind

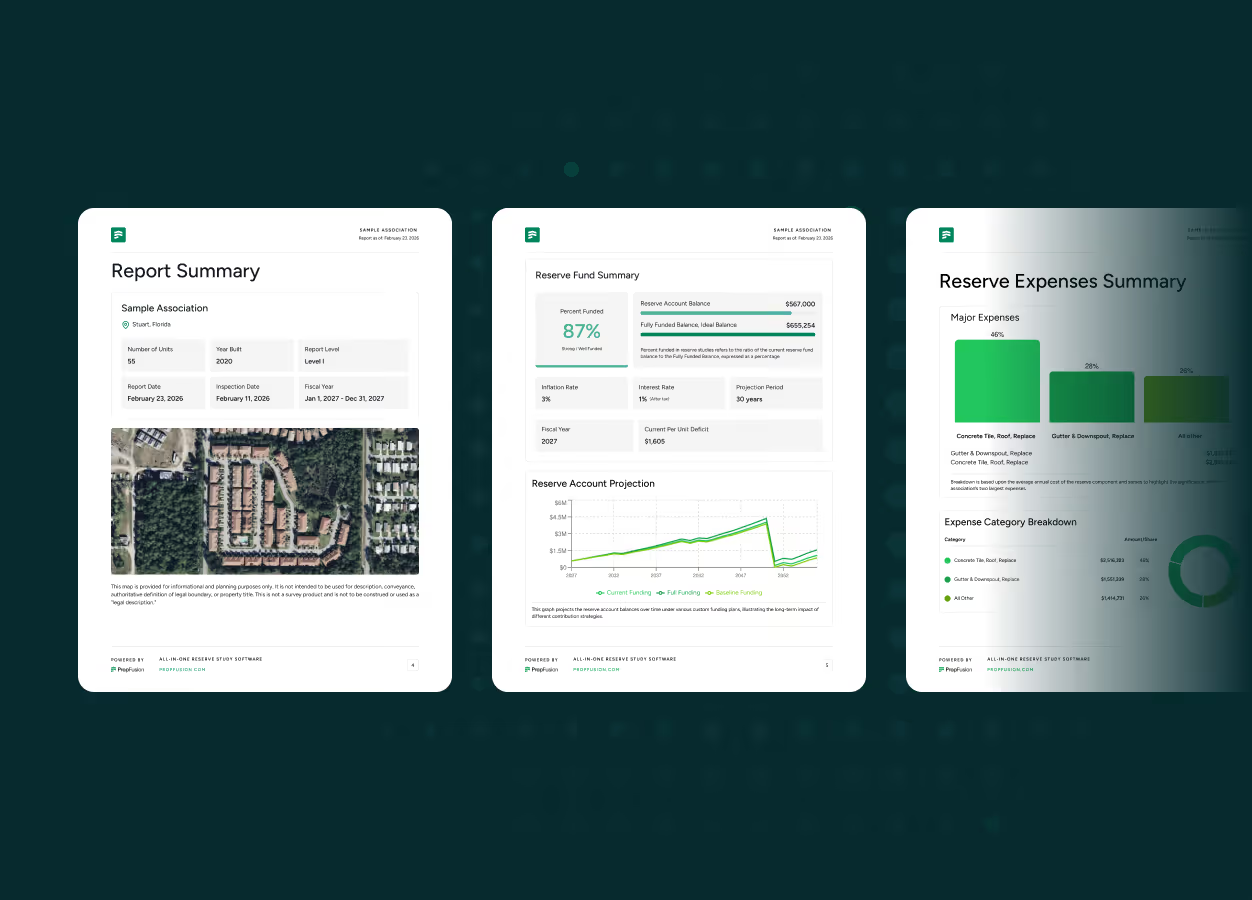

New Jersey’s structural integrity and reserve funding laws exposed an uncomfortable reality. When boards ordered capital reserve studies under N.J.S.A. 45:22A-44.2, many discovered that reserves were nowhere near “adequate.”

The updated rules now require:

- A capital reserve study that meets National Reserve Study Standards.

- At least one 30-year funding plan where the reserve balance can reach zero but never goes negative. This is the baseline or zero-dollar plan.

- Professional updates at least every five years.

For existing associations that are badly underfunded, the key questions are:

- How fast do we have to catch up.

- How can we phase increases so we do not destroy cashflow.

This article explains what the law expects and shows how a 10-year catch-up horizon can work in practice.

What the law says about catching up

There are three concepts boards need to understand.

1. Adequate funding and the zero-dollar plan

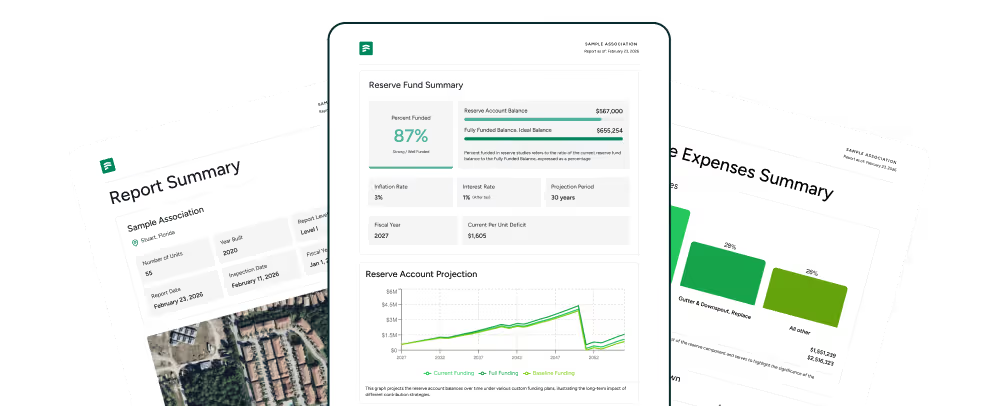

Amendments adopted through S3992 define “adequate” funding around a 30-year plan that never lets the reserve balance fall below zero. The reserve study must include that zero-dollar plan and may include other plans with higher minimum balances or escalating contributions, as long as none of them project a negative balance.

In plain language: whatever catch-up path you choose, by the end of the planning horizon your association must be on a baseline track where reserves stay above zero without relying on constant emergency assessments.

2. Ten-year catch-up guidance in early commentary

Early commentaries on S2760 explained that if moving to adequate funding required more than a 10 percent increase in common expense assessments, associations could phase that increase in over up to ten fiscal years with equal annual steps. If the increase needed was 10 percent or less, the law expected compliance within two fiscal years.

Later legislative updates removed the specific “two- and ten-year” language, but they did not forbid phased increases. Law-firm and industry FAQs still talk about ten-year catch-up plans because they remain a practical planning horizon for communities that start far behind.

In this article, “10-year catch up” is a practical planning frame that fits within the updated baseline and 85 percent rules, not a guaranteed safe harbor.

3. The temporary 85 percent funding option

Under S3992, many existing associations may temporarily fund at 85 percent of a chosen reserve funding plan for up to five fiscal years. After that, they must fully fund at least the baseline plan. This 85 percent option comes with strict disclosure requirements, including large-font notices to owners and buyers.

Used carefully, 85 percent funding can form the first half of a ten-year catch-up path. Used carelessly, it simply stores up a bigger assessment in year six.

Step 1: Quantify how far behind you are

Before designing any catch-up plan, your board needs hard numbers.

Ask your reserve professional for:

- Baseline funding plan details in the latest capital reserve study, including year-by-year contributions and balances.

- Current reserve balance and how far it sits below the baseline curve.

- Short-term risk projects in the next five years, such as roofs, facade repairs or garage work, with realistic cost ranges.

Many New Jersey law and engineering firms stress that reserve studies must now be prepared or reviewed by a licensed engineer, architect, or credentialed reserve specialist, and updated at least every five years.

If your last study is older than that, your first task is to commission a compliant update.

Step 2: Choose a realistic catch-up horizon

For a heavily underfunded association, jumping straight to baseline funding in one year could mean assessment hikes of 30 to 50 percent. Boards looking to avoid that shock typically choose one of three horizons:

- Five years where the community can tolerate steep increases.

- Ten years where the goal is to spread pain and align with the life cycle of major projects.

- Hybrid paths where you fund at 85 percent for a few years, then move to 100 percent with a one-time special assessment or loan.

New Jersey commentary on S3992 emphasises that by the end of any transition you must be at baseline funding and that the 85 percent option cannot be used for more than five fiscal years.

Ten years is attractive because it matches how owners think about mortgages and major projects, and it gives time for incomes to catch up to assessments.

Step 3: Design the 10-year path

With your reserve provider, ask for three specific 10-year scenarios that all land at baseline compliance by the end of the window.

Scenario A: Straight-line increases

Here the board adopts equal percentage increases each year for ten years until the association reaches baseline contributions.

Typical features:

- Simple to explain.

- Works well when you are behind but not catastrophically.

- Easier to model inside a platform like PropFusion because the percentage step is constant.

Scenario A is closest to the early “equal annual increase” guidance described in law-firm summaries.

Scenario B: Front-loaded increases with a plateau

This path raises assessments more aggressively for three to five years, then holds contributions relatively flat.

It suits communities that:

- Have near-term structural projects.

- Want to show lenders and insurers that they are closing the gap quickly.

Because near-term balances are higher, Scenario B can reduce the risk of special assessments if a project overruns.

Scenario C: 85 percent funding plus scheduled special assessment

Some communities simply cannot afford a big immediate jump in assessments.

Scenario C uses the statutory flexibility:

- Fund at 85 percent of the baseline plan for up to five years.

- Document a planned special assessment or loan in year five or six.

- Move to 100 percent baseline funding after the catch-up event.

From a risk perspective, Scenario C is the least comfortable, but it may be the only politically viable path in an underfunded association with owners already stretched thin.

Step 4: Decide how to mix monthly assessments, special assessments and loans

New Jersey’s reserve law expects capital projects to be paid from reserves under your 30-year funding plan, but it recognises that some assets will fail earlier than predicted or cost more than expected. In those situations, a special assessment or loan can still be appropriate, as long as the reserve study and funding plan are updated to reflect the reality.

When you review the three scenarios, ask four questions:

- How often do we trigger special assessments and for what size.

- How much room do owners actually have for monthly assessment increases.

- How will lenders and insurers view each scenario.

- Which path best balances fairness between current and future owners.

PropFusion helps on this step because your reserve professional can plug loans, lines of credit and special assessments directly into the model and show you how each choice affects balances and compliance over 30 years.

Step 5: Build owner communication around the 10-year story

Under S3992, associations that use the 85 percent option must give owners a clear written notice that explains the shortfall, the expected catch-up event and the reasons for choosing that path.

Even if you do not use 85 percent funding, you should treat communication as if the law required it.

Practical steps:

- Publish a one-page summary of the reserve study and the chosen scenario.

- Show two simple charts: current path if nothing changes and the proposed 10-year path.

- Explain why a slower catch-up would put the association out of compliance or leave later owners holding the bag.

- Tie messaging back to safety, property values and lender expectations, not just legal compliance.

How PropFusion supports 10-year catch-up plans

New Jersey’s regime turns reserves into an ongoing modelling exercise rather than a one-time report.

With PropFusion, a reserve professional can:

- Import your New Jersey-compliant reserve study and baseline plan.

- Build multiple catch-up scenarios over ten years, including the temporary 85 percent option.

- Show graphs of assessment levels, reserve balances and project timing so boards can see the tradeoffs.

- Keep funding plans updated as projects complete and as the law evolves.

Boards then have a single system where the reserve study, 30-year funding plan and real-world performance stay in sync.

Related Reading

- Who Is Really Exempt from New Jersey Reserve Studies? — Check whether your association qualifies for an exemption.

- What Does Fully Funded Reserves Mean? — Understand the percent funded metric in your reserve study.

- HOA Reserves Rule of Thumb — How much should your association have in reserves?

FAQs: Catching up when your New Jersey association is behind

If we are badly underfunded, do we have to fix everything in one budget year?

No. The law focuses on getting to a baseline 30-year plan where reserves never go negative, not on an overnight fix. Early guidance described two- and ten-year catch-up windows depending on the size of the needed increase, and although that precise language has been removed, law-firm summaries confirm that phased increases remain acceptable as long as you move toward baseline funding and comply with disclosure rules.

How long can we rely on the 85 percent funding option?

Existing associations may adopt a budget that funds reserves at 85 percent of a plan from the capital reserve study for up to five fiscal years. After that, the association must transition to a plan that satisfies the zero-dollar baseline requirement. During the 85 percent period, boards must give prominent written notice to owners and buyers about the shortfall and expected catch-up actions.

Is a ten-year catch-up plan still valid now that S3992 has passed?

Yes, as a planning tool, provided that:

- The plan moves you onto a compliant baseline funding track.

- Any use of 85 percent funding respects the five-year limit.

- Increases are phased in a way that is transparent and documented.

Recent guidance from reserve professionals and New Jersey community association lawyers still uses ten-year projections as a reasonable horizon for underfunded communities that need time to adjust.

What happens if we do nothing and remain underfunded?

DCA materials stress that boards have a fiduciary duty to comply with the capital reserve study and funding requirements. Ignoring them can create exposure if structural problems appear and reserves are inadequate. It also increases the risk of large emergency assessments, difficulty obtaining insurance and problems with buyer financing.

Is this article legal advice?

No. It is practical guidance based on current statutes and industry commentary. Your association should work with New Jersey association counsel and a qualified reserve specialist or engineer to design a catch-up plan that fits your documents, your buildings and your owners.

PropFusion delivers professional reserve studies with 30-year funding plans - powered by modern technology and backed by certified reserve analysts.

Take the guesswork out of your reserve study

PropFusion delivers professional reserve studies powered by industry-leading software. Request a proposal to get started.