What Does Fully Funded Reserves Mean? HOA Funding Explained

Get proposals from vetted reserve study professionals - with 30-year funding plans, powered by modern technology, and compared side by side for free.

When board members and owners ask, “What does fully funded reserves mean?”, they are usually trying to understand whether their HOA has “enough” money set aside for future repairs. On paper, “fully funded” sounds simple – but in reserve planning it has a very specific technical meaning tied to your reserve study and funding objective.

What does fully funded reserves mean?

An association is fully funded when its reserve balance equals the fully funded balance (FFB) calculated in its reserve study — 100% of the deteriorated value of all common components. In practice, 70–100% funded is widely considered a healthy range.

This guide breaks down that meaning in practical terms, explains how Fully Funded Balance and Percent Funded are calculated, and shows how different funding strategies (Full, Threshold, and Baseline) change your risk profile. By the end, you will know how to read these numbers in your own reserve study and what “fully funded” looks like for your community.

What Does “Fully Funded Reserves” Actually Mean?

In reserve planning, “fully funded reserves” does not just mean “we have a lot of money in the bank.” It means that your reserve balance matches the Fully Funded Balance (FFB) calculated in your reserve study for a given point in time.

In plain language:

Your reserves are fully funded when the money you have set aside equals the amount that should have been saved up so far for all major components, based on their cost and wear to date.

Reserve study standards describe this as the depreciated value of your components. Each roof, pavement area, elevator, or other asset has:

- An estimated total replacement cost, and

- A useful life and remaining useful life.

The Fully Funded Balance is the total of what you “should” have saved up to this year for each component, based on how much of its life has already been used.

So:

- If your actual reserve balance ≈ Fully Funded Balance → you are at or near fully funded.

- If your balance is much lower than the Fully Funded Balance → your reserves are underfunded.

- If your balance is higher → you are over the fully funded level.

This is where the metric Percent Funded comes in – it expresses how close you are to that fully funded target as a percentage.

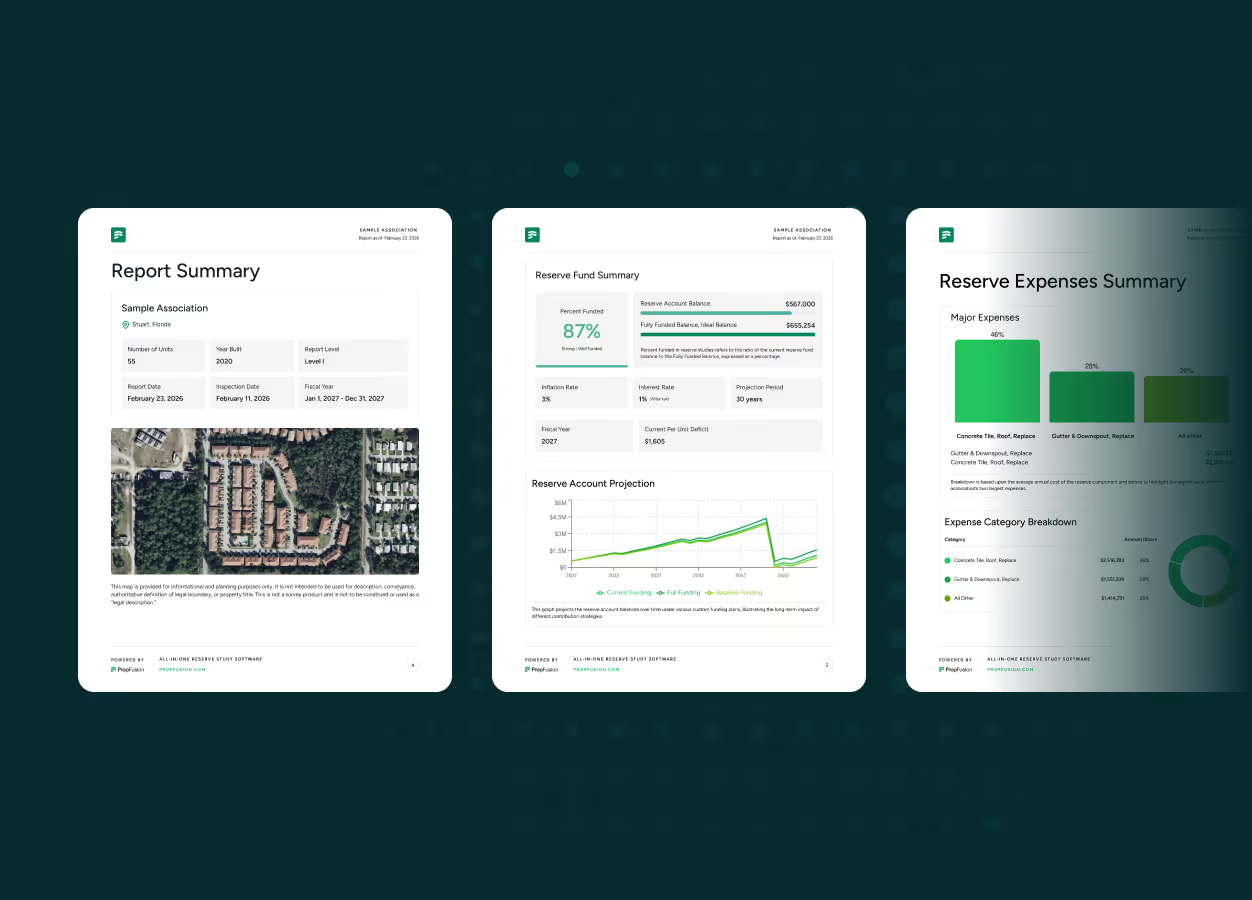

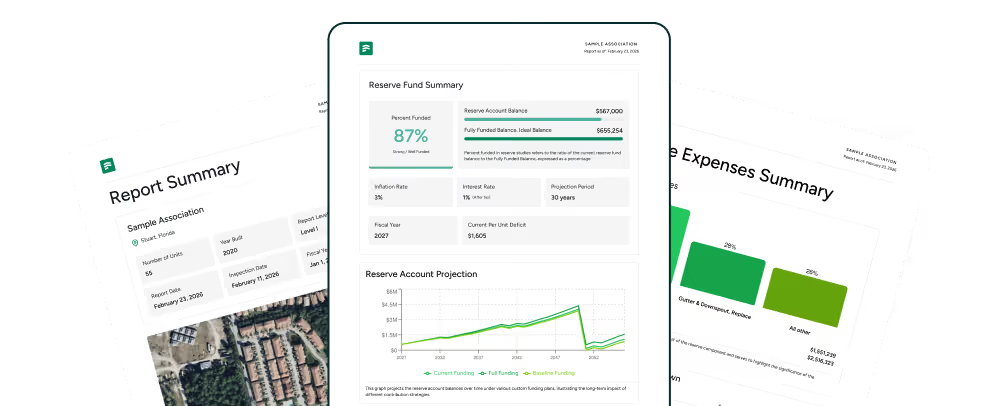

Fully Funded Balance vs Percent Funded: How the Numbers Work

To understand what fully funded reserves mean in practice, you need to understand two related concepts from your reserve study:

- Fully Funded Balance (FFB) – the ideal reserve balance at a given point in time.

- Percent Funded – where you actually stand relative to that ideal.

Fully Funded Balance (FFB)

The Fully Funded Balance is the sum of the “used-up” portion of all of your major components at a specific date.

For each component, the reserve preparer estimates:

- Current replacement cost

- Total useful life (for example, 20 years)

- Remaining useful life (for example, 10 years left)

If a roof costs $100,000 to replace, has a 20-year life, and you are 10 years in, then half its life has been “used.” In a simple straight-line example, the Fully Funded Balance for that one component would be:

- $100,000 × (10 years used ÷ 20-year life) = $50,000

Do that calculation for every component in the study and add the amounts together – the result is the Fully Funded Balance for the whole association this year.

Percent Funded

Percent Funded compares your actual reserve balance to the Fully Funded Balance:

- Percent Funded = (Actual reserve balance ÷ Fully Funded Balance) × 100

Using the simple example above:

- If your actual reserve balance is $50,000 and the Fully Funded Balance is $50,000 → you are 100% funded.

- If your balance is $35,000 with the same Fully Funded Balance → you are 70% funded.

- If your balance is $15,000 → you are 30% funded.

In other words:

- 100% funded = fully funded in the strict standards sense.

- Numbers below 100% tell you how far below that ideal you are.

- Numbers above 100% mean you are ahead of the fully funded level at that moment.

Many professionals talk about funding strength ranges (for example, considering communities in a certain band as “strong” and those far below as “weak”), but those ranges are an interpretation of Percent Funded – not a separate concept. If you want a detailed discussion of “what is a healthy percent funded level” and rule-of-thumb ranges, that belongs in a separate “HOA reserves rule of thumb” guide. This article is about the underlying definitions and funding strategies.

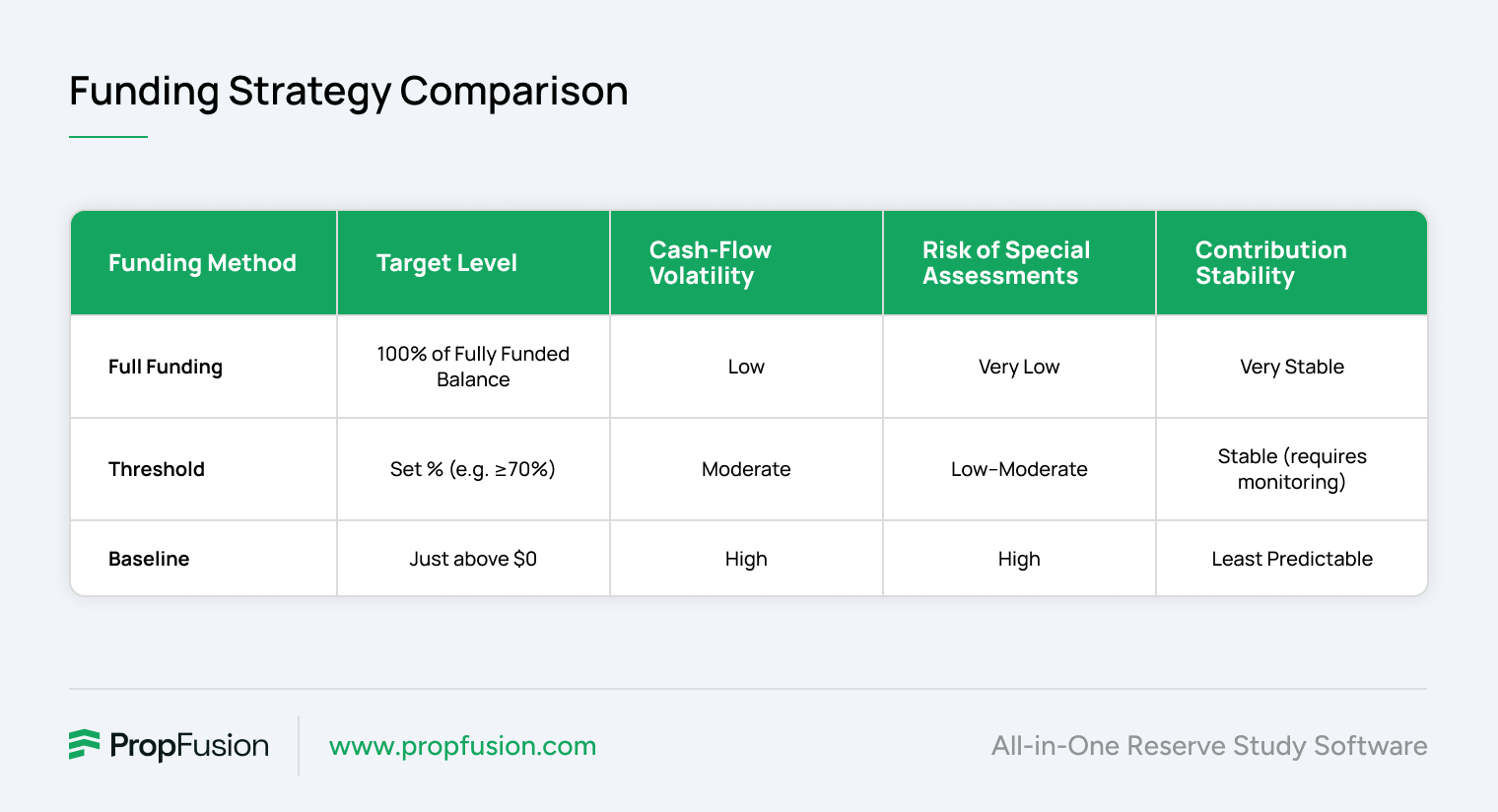

Three HOA Reserve Funding Objectives: Full, Threshold, and Baseline

Knowing what Fully Funded Balance and Percent Funded mean is one thing. Deciding how aggressively you want to fund your reserves is another. That is where funding objectives come in.

Most reserve professionals talk about three main objectives:

- Full Funding

- Threshold Funding

- Baseline Funding

Each objective describes a different target for where you want your reserves to be over time.

Full Funding – Targeting 100% of the Fully Funded Balance

Under a Full Funding objective, the association’s contributions are designed so that:

- The projected reserve balance stays at, or very close to, 100% of the Fully Funded Balance over the life of the study.

In practical terms:

- The community consistently contributes enough each year to keep reserves fully aligned with the depreciated value of its components.

- When a major project (like a roof replacement) occurs, the balance drops as planned, then contributions continue to build reserves back up toward the Fully Funded Balance over the next cycle.

Benefits:

- Maximum resilience against surprises; you rarely need special assessments if forecasts are reasonably accurate.

- Strong optics for buyers, lenders, and regulators – the numbers clearly show that the community is on top of its long-term obligations.

- More flexibility in choosing timing and quality of projects.

Trade-offs:

- Full Funding usually requires higher annual contributions than other objectives.

- In communities sensitive to assessment increases, it can be politically difficult to commit to Full Funding without clear owner communication.

Threshold Funding – Staying Above a Target Floor

Under a Threshold Funding objective, the goal is not to stay at 100% of the Fully Funded Balance at all times. Instead, the association:

- Chooses a minimum target (a “threshold”) for the reserve balance or Percent Funded – for example, staying above a certain band in the funding projections.

- Designs contributions so that the projected reserve balance never falls below that floor.

In practical terms:

- You might accept that your Percent Funded number will move around – for example, between 60% and 90% – but you design the plan so it doesn’t drop into clearly high-risk territory.

- You still rely on a reserve study to set that threshold; it is not an arbitrary guess.

Benefits:

- Lower ongoing contributions than strict Full Funding.

- More room to balance reserve funding with affordability for owners.

- Still offers structure and discipline; you have an explicit line you do not want to cross.

Trade-offs:

- More sensitivity to cost overruns or early failures.

- If actual project costs or timing differ significantly from the study, you can dip below your threshold unless you adjust contributions in time.

For many communities, Threshold Funding is a realistic middle ground between ideal resiliency and what owners will accept in assessments.

Baseline Funding – Avoiding $0 but Accepting More Risk

Under a Baseline Funding objective, the priority is:

- Keeping reserves from dropping to zero (or below) in the projections, rather than maintaining a specific Percent Funded level.

In other words:

- Contributions are set so the projected reserve balance stays just above zero over the life of the study.

- There is no explicit target to be near the Fully Funded Balance; the object is to avoid complete depletion.

Benefits:

- Lowest near-term assessment impact; contributions can be set at a level that is more comfortable for owners in the short run.

- Attractive to boards facing strong resistance to higher dues.

Trade-offs:

- Typically results in low Percent Funded levels, often in ranges that are considered high risk.

- The association has very little margin for error if costs go up, components fail early, or new needs emerge.

- Special assessments, loans, or deferred maintenance become more likely.

Baseline Funding is a governance choice. It is not “wrong” by definition, but it is important that boards and owners understand the increased risk and potential long-term cost.

How to Tell If Your HOA’s Reserves Are Fully Funded

Once you understand these concepts, the next question is straightforward:

How do we know whether our own HOA’s reserves are fully funded or underfunded?

Here is a practical process.

Step 1 – Confirm You Have a Current Reserve Study

First, make sure you are looking at a current reserve study:

- If your study is many years old, your component list, costs, and remaining useful lives may no longer be accurate.

- Significant changes to the property (new amenities, major repairs, additions) should trigger updates.

Without a current study, any conclusion about being fully funded or underfunded is guesswork.

Step 2 – Find the Fully Funded Balance and Percent Funded

Next, locate these two numbers in the report:

- Fully Funded Balance for the current year.

- Percent Funded for the current year.

They are often shown in the funding summary, in tables, and on graphs that plot projected balances over time.

Once you have them:

- If Percent Funded ≈ 100% → you are essentially fully funded in the strict standards sense.

- If Percent Funded is below 100% → you are below the fully funded level by that percentage.

- If Percent Funded is above 100% → your balance exceeds the Fully Funded Balance at this moment in time.

Step 3 – Check What Funding Objective You Adopted

Then, check what funding objective your association is following:

- Did your board adopt a Full Funding objective and instruct the preparer to design contributions around 100% funding?

- Did you choose Threshold Funding, with a stated minimum target?

- Are you following a Baseline Funding plan that simply avoids running out of reserve cash?

A community that intentionally follows Threshold Funding at, say, 70–80% of FFB is not “failing” just because it is below 100%. It is following a different objective with known trade-offs. A community using Baseline Funding may sit at low Percent Funded levels by design, but that should be recognised and communicated as a conscious choice.

Step 4 – Discuss Whether that Objective Still Matches Your Risk Tolerance

Finally, boards should ask:

- Does our current funding objective still reflect our community’s risk tolerance, age, and needs?

- Have construction costs shifted enough that our thresholds need to be revisited?

- Are owners increasingly concerned about special assessments or property values, suggesting a move toward a stronger funding objective?

This is where your reserve professional can model alternate plans and show exactly how different objectives (Full, Threshold, Baseline) affect future assessments and risk.

How to Calculate Your HOA Reserve Fund Needs

Calculating how much your HOA should have in its reserve fund requires three pieces of information:

Step 1: List all reserve components. Identify every major common-area asset the association is responsible for maintaining or replacing — roofs, pavement, pools, HVAC systems, elevators, exterior painting, fencing, and so on.

Step 2: Determine each component's Fully Funded Balance. For each component, calculate: (Current Age ÷ Useful Life) × Replacement Cost = Fully Funded Balance for that component. For example, if a roof has a 25-year useful life, is currently 10 years old, and costs $500,000 to replace: (10 / 25) x $500,000 = $200,000 fully funded balance.

Step 3: Sum all components. Add up the fully funded balance for every reserve component. This total is your association's overall Fully Funded Balance — the ideal amount your reserve fund should hold right now.

Step 4: Calculate your Percent Funded. Divide your actual reserve fund balance by the Fully Funded Balance: (Actual Reserve Balance / Fully Funded Balance) x 100 = Percent Funded. A result of 70-100% is generally considered healthy. Below 30% is considered poorly funded and may indicate risk of special assessments.

While boards can perform rough calculations themselves, a professional reserve study is the most reliable way to get accurate numbers — reserve specialists use site inspections, local construction cost data, and inflation projections that spreadsheet estimates typically miss.

What “Fully Funded” Looks Like in Practice

It can help to look beyond formulas and think about what fully funded reserves look like in daily HOA life. Consider three simplified scenarios.

Scenario A – Full Funding Objective, High Percent Funded

This community:

- Adopts a Full Funding objective.

- Keeps Percent Funded close to 100% over time.

- Updates its reserve study regularly and adjusts contributions based on updated forecasts.

In practice:

- Major projects (roof replacements, asphalt overlays, repainting) are planned several years in advance.

- Special assessments are rare and generally tied to extraordinary, unplanned events.

- Owners see stable, gradually increasing assessments rather than sudden spikes.

- Lenders and buyers view the association’s financials as a positive.

Scenario B – Threshold Funding Objective, Strong Mid-Range Percent Funded

This community:

- Adopts a Threshold Funding objective, for example committing to stay above a certain Percent Funded band or balance.

- Is comfortable running between, say, 60% and 90% funded over time.

- Uses the reserve study to adjust contributions whenever projections approach the threshold.

In practice:

- Annual contributions are lower than in Scenario A, but still disciplined.

- The board may occasionally increase assessments or adjust the plan to stay above its chosen floor.

- Risk is moderate; there is some buffer, but not as much as under Full Funding.

- Owners get more affordability in exchange for accepting some additional risk.

Scenario C – Baseline Funding Objective, Low Percent Funded

This community:

- Adopts a Baseline Funding objective that avoids zeros in the projections.

- Often runs at low Percent Funded levels.

- Uses reserve contributions mainly to keep cash from running completely dry.

In practice:

- Regular dues appear lower than peers in the near term.

- When large projects hit sooner than expected or costs surge, the board may need to impose special assessments or take loans.

- Deferred maintenance becomes more likely if owners resist those measures.

- Buyers, lenders, and some owners may see the low reserve strength as a red flag.

All three scenarios can be managed, but only if everyone understands the funding objective and its consequences. “Fully funded reserves” is not just a number – it is a reflection of the strategy the board has chosen.

Reserve Funds vs Operating Funds: A Quick Reminder

Because Fully Funded Balance and Percent Funded relate only to reserve funds, it is important not to confuse reserves with operating funds.

- Operating fund: covers recurring, day-to-day expenses – utilities, landscaping, insurance, management, routine maintenance, admin.

- Reserve fund: covers major future repairs and replacements – roofs, asphalt, painting, mechanical systems, amenities.

Operating budgets look at one year at a time; reserve planning looks at decades. Fully funded reserves are measured only against the long-term capital needs in your reserve study, not against your operating expenses.

If you need a deeper refresher on the difference between these two funds, it is better handled in a separate HOA Reserve Funds 101 article. Here, the key is simply to remember that “fully funded reserves” is about the long-term capital side of your finances, not the operating budget.

Related Reading

- HOA Reserves Rule of Thumb — How much should your association set aside each year?

- Underfunded Reserves: Recovery Plans for HOAs — Steps to close a reserve funding gap.

- The 3 Types of Reserve Studies — Full, update, and no-site-visit studies explained.

- Reserve Study Laws by State — See what your state requires for reserve planning.

Frequently Asked Questions

What does “fully funded reserves” mean in an HOA?

In an HOA, fully funded reserves mean your reserve balance is equal to the Fully Funded Balance calculated in your reserve study for a given year. That balance represents the amount that should have been saved so far for all major components, based on their cost, useful life, and how much of that life has already been used. When your actual balance equals that target, you are 100% funded.

Is an HOA required to be 100% funded?

In most jurisdictions, laws focus on whether associations prepare and disclose reserve studies and funding information, rather than requiring a specific Percent Funded level. There is no universal legal requirement that every HOA must be 100% funded at all times. Instead, boards choose a funding objective (Full, Threshold, or Baseline) and work with their reserve professional to design a plan that matches their risk tolerance, governing documents, and any applicable state rules.

What’s the difference between Fully Funded Balance and Percent Funded?

The Fully Funded Balance is the ideal reserve balance at a point in time, based on component costs and how much of their useful life has been used. Percent Funded tells you where you actually stand relative to that ideal by dividing your actual reserve balance by the Fully Funded Balance and expressing the result as a percentage. Fully Funded Balance is the target; Percent Funded is the score.

Can a community choose Threshold or Baseline funding and still be financially healthy?

Yes – many communities consciously choose Threshold Funding and operate in a healthy mid-range Percent Funded band because it balances risk and affordability. Even Baseline Funding can be a deliberate strategy if owners understand and accept the higher risk of special assessments and the need for more frequent plan adjustments. What matters is that the funding objective is clear, based on a current reserve study, and revisited regularly – not that every association pursues 100% funding at all times.

What happens if reserves are over 100% funded?

If your Percent Funded number is above 100%, it means your current reserve balance is higher than the Fully Funded Balance at that moment. That is not inherently a problem. In some cases, it reflects conservative past funding or favourable project timing. Boards in this position may decide to keep contributions where they are, adjust them gradually, or enhance projects – but any change should still be grounded in updated studies and long-term plans, not a short-term reaction to a single number.

How often should we revisit our funding objective?

Funding objectives and contribution levels should be revisited whenever you update your reserve study or experience major changes in the community. Many associations commission a new or updated study every few years, or as required by their state. Review the funding plan with the reserve preparer and management annually during the budget process. Revisit the objective (Full, Threshold, Baseline) if owners’ expectations, property conditions, or legal requirements change. A funding objective is not set in stone. It should evolve as your community ages, your risk tolerance changes, and better information becomes available.

Get proposals from vetted reserve study professionals - with 30-year funding plans, powered by modern technology, and compared side by side for free.

Take the guesswork out of your reserve study

PropFusion matches your association with vetted reserve study professionals - powered by industry-leading software. Compare multiple proposals for free to get started.