New Jersey Reserve Study Law: S2760 & S3992 Compliance Guide (2026)

New Jersey's Planned Real Estate Development Full Disclosure Act (PREDFDA), amended by Senate Bills S2760 and S3992, requires condominium and HOA communities to complete a reserve study and maintain adequately funded reserves. The law applies to associations with major structural components and imposes specific deadlines, funding thresholds, and reporting requirements.

What does New Jersey's reserve study law require?

Under PREDFDA as amended by S2760 and S3992, New Jersey condominium, HOA, and cooperative associations must complete a capital reserve study — a condominium reserve fund study for shared structural components — keep it current, and maintain adequately funded reserves, with specific deadlines and funding thresholds set by the law.

See the full reserve study requirements by state guide

This guide covers who must comply, what the study must include, key deadlines, cost ranges, and step-by-step compliance guidance under the 2026 law.

Legislation Link

S2760 — Reserve Study Requirements (2022 session)

S3992 — Amendments to Reserve Study Law (2024 session)

PREDFDA Original Act — N.J.S.A. 45:22A-21 et seq.

Are reserve studies required in New Jersey for condos and HOAs?

Yes. Under S2760 (effective January 2024), all common-interest communities governed by PREDFDA must complete a reserve study. The study must be conducted by a qualified professional and updated on a schedule tied to the community's reserve balance and building age.

What is the 85% funding threshold?

S3992 introduced a key provision: associations that maintain reserves at or above 85% of the recommended level in their reserve study are considered "adequately funded." Those below 85% must adopt a baseline funding plan to reach adequacy within 10 years.

How much does a reserve study cost in New Jersey?

In New Jersey, reserve study costs typically range from $3,000 to $8,000 for small to mid-size communities and $8,000 to $15,000+ for large or complex developments. Factors include the number of units, building age, and structural components requiring assessment.

Get proposals from vetted reserve study professionals - with 30-year funding plans, powered by modern technology, and compared side by side for free.

Why New Jersey's Reserve Study Law Matters

New Jersey became one of the most proactive states for reserve fund regulation when Governor Murphy signed S2760 into law in January 2024. The law directly addressed the growing problem of underfunded reserves across the state's aging condominium and HOA communities.

Before S2760, New Jersey had no statewide requirement for reserve studies. Boards had full discretion over whether to plan for future repairs — and many chose not to, leading to deferred maintenance crises and sudden special assessments that blindsided homeowners.

The PREDFDA Connection

S2760 amended the Planned Real Estate Development Full Disclosure Act (PREDFDA), the foundational statute governing common-interest communities in New Jersey (N.J.S.A. 45:22A-21 et seq.). PREDFDA originally focused on disclosure requirements for developers selling units in planned communities.

The 2024 amendment expanded PREDFDA's scope to include ongoing reserve fund obligations for associations — a significant shift from developer-focused disclosure to community-focused financial planning.

Who Must Comply With the NJ Reserve Study Law

The law applies to all common-interest communities governed by PREDFDA. This includes condominiums, planned unit developments (PUDs), and cooperative housing associations with shared structural components.

Specifically, any association responsible for maintaining major structural components — including roofs, building exteriors, roads, drainage systems, and recreational facilities — must conduct a reserve study.

Exemptions

Not every community is subject to the law. The following are generally exempt:

- Communities with fewer than 10 units — Small associations with limited shared infrastructure

- Associations with no major structural responsibilities — Communities where owners maintain all structural elements individually

- Time-share developments — Governed by separate New Jersey statutes

Boards that believe they qualify for an exemption should document their reasoning in writing and consult legal counsel. For a deeper analysis, see our guide on who is really exempt from New Jersey reserve studies.

The 85 percent funding option: flexibility with strings attached

One of the most important changes for boards is the new 85 percent funding option. S3992 allows an association to fund as little as 85 percent of the reserve contribution recommended by the capital reserve study for up to five fiscal years. However, this option is tightly regulated:

- Before adopting a budget that funds reserves at 85 percent of the chosen plan, the board must send a notice to all unit owners, in at least 20-point bold font, clearly stating that it has elected to fund at 85 percent of the recommended amount.

- The notice must disclose the year in which a special assessment or loan is anticipated as a result of this underfunding and the expected amount.

- Any unit owner selling a unit during that 85 percent funding period must provide prospective buyers with the board’s notice regarding the underfunded plan.

- The association may only use the 85 percent funding option for five fiscal years. After that, it must fully fund the chosen reserve funding plan.

Practically, this means the 85 percent option is a short-term pressure valve, not a permanent discount. Boards that use it should do so with eyes open, understanding that it shifts costs into the future and may make units less attractive to buyers if a large special assessment is expected.

What “adequate” reserves mean after S3992

Initially, S2760 required associations to maintain “adequate” reserves but did not define the term. This led to confusion and concern about how aggressively boards would have to increase assessments.

The 2025 amendment S3992 addresses this by defining “adequate” or “adequacy” as a funding plan in which the projected balance of the reserve account does not fall below zero at any point in the 30-year funding projection.

In practice, this means:

- Your funding plan can allow the reserve balance to drop to zero in some years, but never negative.

- You are not required to maintain a fixed minimum reserve balance (for example, one year of expenses) unless your association chooses to adopt a stricter internal standard.

- The professional preparing your reserve study must include a “baseline” funding plan that complies with this no-negative-balance test.

This is a more flexible framework than some feared. Boards still must confront underfunding, but the law explicitly allows a well-structured plan that uses the reserve account efficiently over time, as long as the balance never dips below zero in the projection.

Interaction with structural integrity inspections

The same legislation that created the capital reserve study requirements also introduced stringent structural inspection obligations for certain “covered buildings,” particularly mid- and high-rise condominium and cooperative structures.

Even where a particular building is exempt from structural inspections, the DCA’s FAQ makes it clear that the capital reserve study obligations under 45:22A-44.2 and 44.3 still apply to the association as a whole, provided it is a PRED and meets the asset threshold.

For boards, the takeaway is simple: do not assume that you are exempt from reserve study requirements just because your property is low-rise or otherwise outside the structural inspection rules. The reserve law stands on its own and is designed to ensure you can fund the repairs your future inspection reports will identify.

Practical steps for New Jersey boards to comply

To comply with New Jersey reserve study law and protect both the association and board members, we recommend a deliberate, staged approach:

Step 1 - Confirm whether your association is covered.

If you are a condominium or cooperative, you should assume you are covered. If you are an HOA, have your manager, reserve professional, or attorney confirm whether you are a PRED with at least $25,000 in common area capital assets. Err on the side of compliance unless a professional clearly advises otherwise.

Step 2 - Commission a compliant capital reserve study.

If your last reserve study is more than five years old, or if you have never completed one, engage a CAI Reserve Specialist (RS) or New Jersey-licensed engineer or architect with reserve study experience. Confirm in writing that they will follow the National Reserve Study Standards and include all legally required elements (physical analysis, cost estimates, structural-related items, and a 30-year funding plan).

Step 3 - Review funding options with your professional.

Ask your reserve specialist to present at least one fully adequate funding plan (no projected negative balances) and, if necessary, alternative plans that make use of the phased catch-up rules or the 85 percent funding option. Discuss the trade-offs between higher assessments now versus special assessments or loans later.

Step 4 - Document board decisions and owner communication.

Whatever funding strategy you choose, document the board’s reasoning in meeting minutes. If you adopt the 85 percent option, ensure your notices comply with the 20-point bold requirement and clearly explain the consequences for unit owners and buyers. This documentation will be critical if your decisions are later challenged.

Step 5 - Integrate the study into budgeting and project planning.

Use the reserve study as a live planning tool, not a one-time report. Align your annual budget, upcoming projects, and long-term contracts with the 30-year funding plan. When conditions change (major repair, inflation spike, or scope changes), update the study earlier than required instead of waiting the full five years.

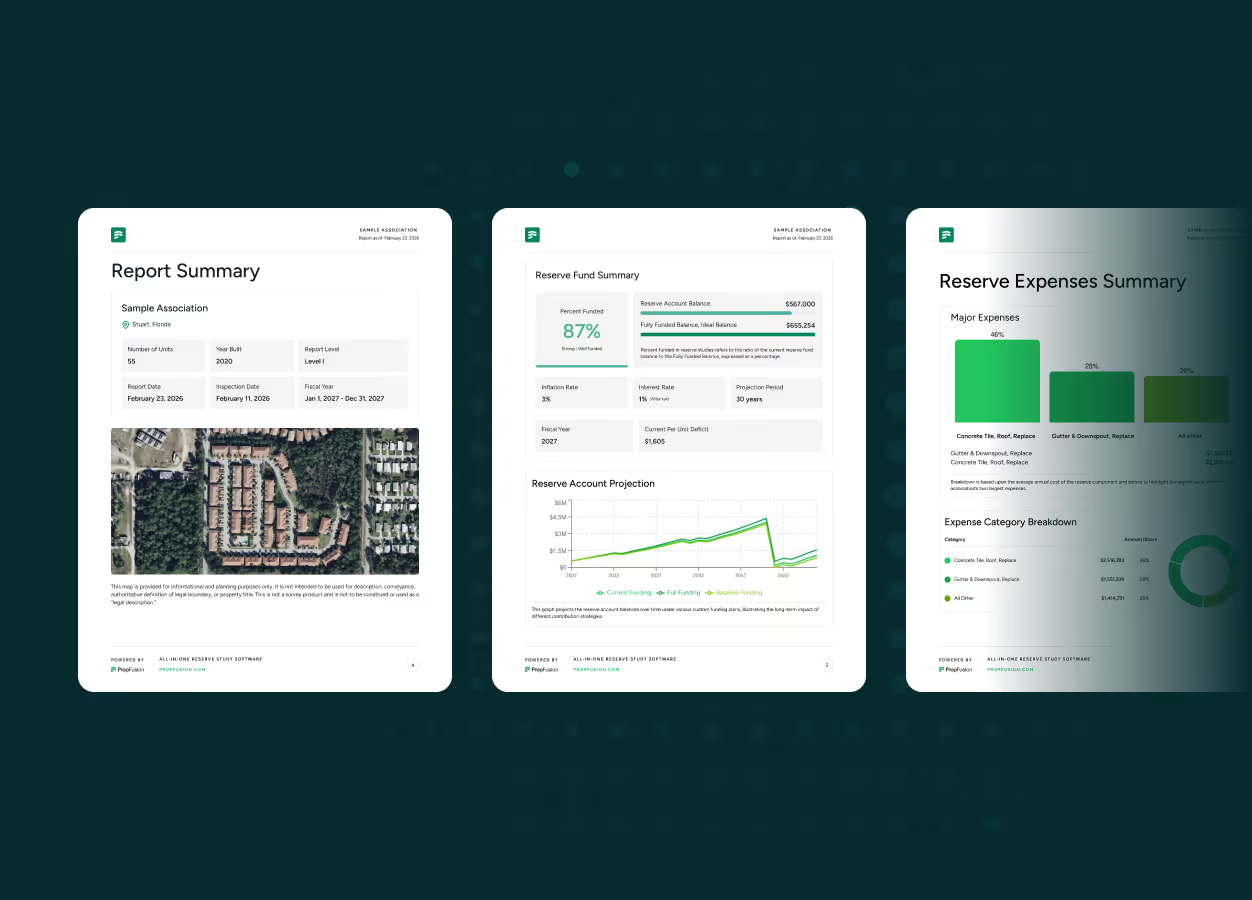

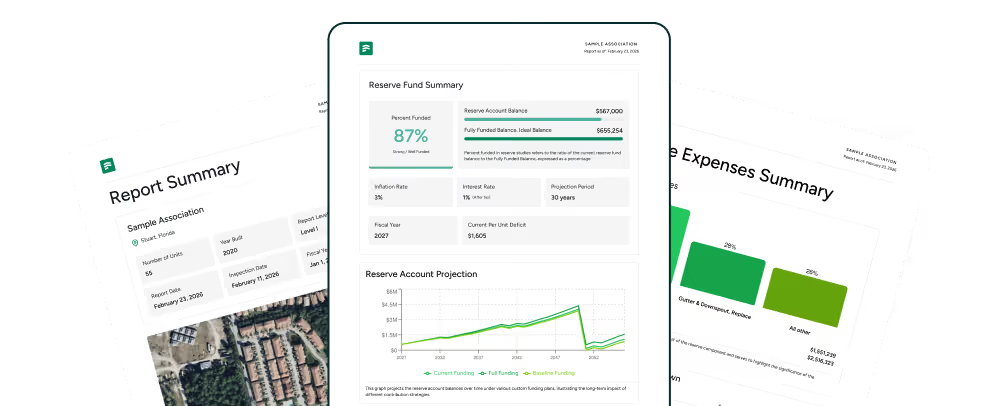

What a New Jersey Reserve Study Must Include

S2760 specifies that the reserve study must be conducted by a qualified professional — typically a reserve study specialist, licensed engineer, or credentialed reserve analyst (RS or PRA designation). The study must inventory all major components and project their replacement costs over time.

Required elements include:

- Component inventory — A complete list of all common-area components the association is obligated to maintain, repair, or replace

- Condition assessment — Current physical condition of each component, including remaining useful life estimates

- Replacement cost projections — Estimated cost to repair or replace each component, adjusted for inflation

- Funding analysis — Current reserve balance, recommended annual contributions, and projected fund balance over a 20–30 year horizon

- Percent-funded calculation — The ratio of current reserves to the ideal balance, expressed as a percentage (learn what fully funded means)

The study must distinguish between Level I (full on-site inspection with financial analysis), Level II (update with on-site inspection), and Level III (update without inspection). New Jersey's initial study requirement calls for a Level I study. Learn more about the three types of reserve studies.

NJ Reserve Study Deadlines and Update Schedule

The law establishes a tiered deadline structure based on when the association was formed and the age of its buildings. Associations that existed before January 2024 had an initial compliance window that has since closed for most communities.

Key timing requirements:

- Initial study — Must be completed within the first year after formation for new associations, or by the deadline specified for existing ones

- Updates — Required at least every 5 years for communities in good financial standing

- More frequent updates — Associations below the 85% funding threshold may need to update more often as part of their baseline funding plan

- Post-catastrophe updates — Required after any major event (hurricane, fire, structural failure) that materially changes component conditions

S3992, signed in 2025, refined these timelines and gave associations additional flexibility to align updates with their fiscal year. Boards should calendar the next update date immediately after receiving their current study.

The 85% Funding Threshold and Baseline Funding Plans

One of the most important provisions in S3992 is the 85% funding adequacy standard. An association is considered adequately funded if its reserve balance is at or above 85% of the amount recommended in its reserve study.

If a community falls below 85%, the board must adopt a baseline funding plan — a written strategy to reach the 85% threshold within 10 years through increased annual contributions.

What the 85% Rule Means in Practice

If your reserve study recommends a balance of $500,000 and your current reserves are $350,000, you're at 70% funded — below the threshold. The board must adopt a plan to reach $425,000 (85%) within 10 years.

This typically means increasing annual reserve contributions by a set dollar amount each year. The law does not require communities to be 100% funded, but boards should understand that 85% is the minimum standard — not the goal. For recovery strategies, see our guide on how underfunded NJ associations can catch up over 10 years.

How Much Does a Reserve Study Cost in New Jersey?

Reserve study pricing in New Jersey varies based on community size, building complexity, and the type of study (Level I vs. update). Below are typical ranges based on PropFusion's experience serving NJ communities.

Factors that increase cost include multi-building campuses, pools and recreational facilities, parking structures, and buildings with complex mechanical systems (elevators, HVAC plants). Communities with more than 200 units or aging infrastructure over 25 years old typically fall at the higher end of each range.

For a detailed breakdown of pricing factors, see how much HOA reserve studies cost.

Transition Studies for New Developments

A transition study is a specialized reserve study conducted when a developer hands control of a community to its homeowner association. This is one of the most important — and most overlooked — studies in a new community's lifecycle.

In New Jersey, the developer turnover process is governed by PREDFDA and triggers specific reserve fund obligations. The transition study establishes the baseline condition of all common elements and determines whether the developer's initial reserve fund contribution is adequate.

Why Transition Studies Matter

Developers often underfund initial reserves to keep HOA fees low during the sales period. A transition study reveals the true funding gap and gives the new board a realistic picture of upcoming capital expenses.

If your community is approaching or going through developer turnover, request a Level I transition study before accepting the reserve fund from the developer. For questions to ask before hiring a firm, see questions NJ boards should ask before hiring a reserve specialist.

How Structural Inspections Relate to Reserve Studies

New Jersey's S2760 also introduced structural inspection requirements for certain buildings. These inspections are separate from — but closely related to — the reserve study.

A structural inspection evaluates the physical integrity of load-bearing elements: foundations, structural frames, balconies, parking decks, and waterproofing systems. The reserve study then uses inspection findings to project repair and replacement costs.

Sequencing Inspections and Reserve Studies

The most efficient approach is to complete the structural inspection first, then commission the reserve study. The inspection findings feed directly into the reserve study's component conditions and cost projections, producing a more accurate funding plan.

Some associations make the mistake of conducting the reserve study before the structural inspection, which can result in understated repair costs and an inadequate funding plan.

Insurance and Lending Implications

Reserve fund adequacy increasingly affects insurance premiums and mortgage lending for NJ condominium communities. Insurance carriers now review reserve study reports when underwriting master policies — associations with underfunded reserves may face higher premiums or coverage restrictions.

On the lending side, Fannie Mae and FHA require condominium projects to demonstrate adequate reserves for project approval. Communities that cannot show a current reserve study or that fall below recommended funding levels may lose their lending eligibility, making it harder for unit owners to buy and sell.

Step-by-Step Compliance Checklist

Follow this sequence to ensure your association meets all NJ reserve study requirements:

- Determine applicability — Confirm your community is governed by PREDFDA and has major structural components requiring reserve funding

- Hire a qualified professional — Select a reserve study provider with RS, PRA, or PE credentials and NJ experience (use our preparation checklist)

- Complete structural inspection — If your buildings require inspection under S2760, complete this before the reserve study

- Commission the Level I reserve study — Ensure it covers all required elements: component inventory, condition assessment, cost projections, and funding analysis

- Evaluate percent-funded status — Determine whether your reserves meet the 85% adequacy threshold

- Adopt baseline funding plan if needed — If below 85%, create a written 10-year plan to reach adequacy

- Incorporate into annual budget — Adjust reserve contributions to match the study's recommendations

- Distribute to homeowners — S3992 requires that a summary of the reserve study be provided to all unit owners

- Calendar the next update — Schedule the next reserve study update per the required frequency (minimum every 5 years)

- Maintain records — Keep all reserve studies, funding plans, and board resolutions on file for future reference and regulatory compliance

PropFusion produces reserve studies for New Jersey communities of all sizes. Our reports meet all S2760 and S3992 requirements and include a clear funding roadmap your board can implement immediately.

Related Resources

Explore these guides for deeper information on topics covered in this page:

- How Underfunded New Jersey Associations Can Catch Up Over 10 Years

- Who Is Really Exempt From New Jersey Reserve Studies?

- Questions NJ Boards Should Ask Before Hiring a Reserve Specialist

- How Much Do HOA Reserve Studies Cost?

- What Does Fully Funded Reserves Mean?

- Three Types of Reserve Fund Studies (Level I, II, III)

- Reserve Study Preparation Checklist for HOAs and Managers

Related reserve study resources for New Jersey

Compare reserve study laws in nearby states, or find help running one for your association:

FAQ

Are reserve studies required in New Jersey?

Yes. Senate Bill S2760, signed into law in January 2024, requires all common-interest communities governed by PREDFDA to complete a reserve study. The law applies to condominiums, planned developments, and cooperative associations with major structural components.

What law governs reserve studies in New Jersey?

New Jersey reserve studies are governed by the Planned Real Estate Development Full Disclosure Act (PREDFDA), as amended by S2760 (2024) and S3992 (2025). The statutes are codified at N.J.S.A. 45:22A-21 et seq.

How much does a reserve study cost in New Jersey?

Reserve study costs in New Jersey typically range from $3,000 to $8,000 for communities with 10–75 units and $8,000 to $15,000+ for larger or more complex developments. Pricing depends on the number of units, building age, and the number of structural components requiring assessment.

How often must a reserve study be updated in NJ?

Reserve studies must be updated at least every 5 years for communities in good financial standing. Associations below the 85% funding adequacy threshold may need more frequent updates as part of their baseline funding plan.

What is the 85% funding threshold?

Under S3992, associations with reserves at or above 85% of the amount recommended in their reserve study are considered adequately funded. Communities below 85% must adopt a baseline funding plan to reach that level within 10 years.

What is a transition study in New Jersey?

A transition study is a specialized reserve study conducted when a developer hands control of a community to its homeowner association. It establishes the baseline condition of all common elements and determines whether the developer's initial reserve fund contribution is adequate.

Who is exempt from the NJ reserve study requirement?

Communities with fewer than 10 units, associations with no major structural responsibilities, and time-share developments are generally exempt. Boards that believe they qualify for an exemption should document their reasoning in writing and consult legal counsel.

What is the difference between a reserve study and a structural inspection?

A structural inspection evaluates the physical integrity of load-bearing building components. A reserve study projects the long-term costs of maintaining and replacing all common-area components and recommends annual funding contributions. The inspection findings should inform the reserve study's cost projections.

What happens if our association does not comply with S2760?

Non-compliant associations face potential legal liability from unit owners, difficulty obtaining adequate insurance coverage, and loss of Fannie Mae or FHA lending eligibility for the community. Boards that fail to commission a study may also face personal liability for breach of fiduciary duty.

Can we use our existing reserve study to satisfy the new NJ law?

Possibly. If your existing study was completed by a qualified professional, includes all required components (inventory, condition assessment, cost projections, funding analysis), and is less than 5 years old, it may satisfy the law's initial requirement. However, it must also address the 85% funding adequacy threshold introduced by S3992.

The information contained on this page is provided for informational purposes only, and should not be construed as legal advice on any subject matter. You should not act or refrain from acting on the basis of any content included on this page without seeking legal or other professional advice. The contents of this page contain general information and may not reflect current legal developments or address your situation. We disclaim all liability for actions you take or fail to take based on any content on this report.

Get proposals from vetted reserve study professionals - with 30-year funding plans, powered by modern technology, and compared side by side for free.

Take the guesswork out of your reserve study

From site inspection to 30-year funding plan, PropFusion handles the entire reserve study - accurate, transparent, and built on modern technology that gives you full control over your reserves.